Goodwill Hunting

When you think you've solved the math of valuations, but really, you should stick to being a janitor...

I'm writing this article in between drafts of another article that's coming up detailing my past, simply because i want to take my time on that one, and i found another interesting thing to talk about. It's been a while since i wrote my last article (due to my work on starting up my own company and the stress that brings) and i thought this made a nice subject as a little tide-over.

Last April, i did some research into Cathie Wood and her Ark brand of ETFs after learning that she was pursuing a strategy of owning more than 10% of companies, in highly-speculative plays none the less, and i wanted to see how deep that rabbit hole went. After finding out she was indeed a blithering idiot, it is during this research where i first noticed this particular anomaly - and decided to write this article after finding it again in a completely different and unrelated stock in a recent stream, leading me to believe many more companies have pulled this crap. The Twitter thread i made on the basis of that research can be found here:

Since that thread, ARKK is down - alot - and this strategy hasn't done well for Cathie. As far as i know, nothing's changed much, and the issues i highlighted in that Twitter thread still persist for pretty much all companies mentioned.

The way i analyze companies quickly when i have to go through an entire list of them is the same as anybody who goes through alot of companies, and it's a reason i bring up the thread, because it's a skill that's woefully underpracticed these days:

Balance sheet analysis.

Simple balance sheet analysis can save you a WORLD of pain, and it doesn't have to take long. For each of those companies on that list, i didn't spend more than 5 minutes on each balance sheet. The entire thread took mere hours to compile. And i could still find issues easily that would immediately put any investor off - also proving Cathie doesn't actually do any balance sheet analysis. Which was partly the point of the thread.

While i won't go through every company again (though i'll highlight another specifically insane example later as well as a few more obvious stupid bets), there is one in particular i wished to highlight, as it employs the same tactic to pump up its value as the company i analyzed during the stream. It also happens to be Cathie's biggest holding aside from Tesla inside of ARKK (while i'd never heard of it before looking at ARKK), which is how i ran across it.

That company is ofcourse, Teladoc Health.

On April 14th when i looked at ARKK's holdings (and the other ETFs as well as Cathie has a tendency to buy the same stocks with multiple ETFs), Teladoc was in 4 ETFs (still is) to the tune of 13,75 million shares. Since that date, the share price has fallen by close to half, and current Ark holdings are 16,29 million shares, still valued at $2,25 billion total (compared to $2,5 billion in April). Courtesy of https://arktrack.com/:

The increase in holdings should come as no surprise, as i already called her an idiot. However, it's this "Value" number i want to talk about, because few people seem to understand what a market cap is these days, and almost none understand value.

The market cap of a company is simple: Amount of shares times price per share. That's it. If you read about market cap increases, that's simply because large numbers get clicks faster in this day and age. Especially when Tesla increases by several billion market cap in a day. And while that is kind of a problem - when you have slightly over 1 billion shares outstanding, the moment the share price moves up $1, the market cap moves up an entire billion.

It can fall as fast as it goes up, yknow. Just gets reported on less when it does.

On crypto by the way: same thing. The market caps are calculated by taking the current coin price (in dollars, mind you), times the current amount of coins outstanding. This tells you absolutely nothing about USD liquidity. Coins can still go to zero very easily - even Bitcoin - and take the entire market cap down with them.

When Arktrack says "value", what they actually mean is "amount of shares owned times the price of one share". 16,290,919 shares times $138.63 is $2,258 billion. You'll notice from comparing screenshots by the way that Arktrack hasn't been updated in quite a while, which is a shame. Hence the theory lesson, as we can now simply calculate that, if Ark hasn't decreased its overall holdings (which is unlikely at this point), 16,29 million shares times the current shareprice of $102.05 = $1,662 billion in "value" left.

I'm not gonna calculate the amount of money lost here, as that's not my point. My point is, what REALLY is value then, if it clearly can't be learned from the market cap or share price.

Well, that's why balance sheet analysis exists. It doesn't exist as much to find value within a company - you're much better off just reading quarterlies and analyzing the company's news feed, which i do quite often as well. But it does exist for you to find discrepancies that point to the value proposed by the company being a lie. Shareholders actually have quite a few legal protections, and one of them is that the company must be honest towards its shareholders. They MUST tell them everything, even the bad stuff.

They might manipulate what's on the balance sheet by shifting it around, hiding bad assets in categories you wouldn't expect them to be (*cough*Evergrande*cough*Inventory*hack*), but if the board didn't disclose something to the shareholder at all.... they're in much more trouble. CEO's aren't personally liable for alot of things, but hiding stuff from shareholders, very much so.

A person versed in balance sheet analysis will always be able to find the hidden risks within a company.

No calls on hidden risks outside of the company though. But i never said one should only engage in balance sheet analysis - only that one should as part of the toolset.

So lets engage in some analysis then. And i can tell you - a massive amount of people who say they do balance sheet analysis, only look at revenues, and nothing else. Using that as an example, Teladoc seems to be doing very well indeed! (with thanks to Seeking Alpha):

Wow look at that! Their last revenue growth is listed as being 114%! Who wouldn't wanna invest in a company like that?

...anybody who looks slightly further. Literally to the paragraph straight below it.

Purely on the basis of this table alone will i call Cathie Wood a complete blithering idiot who doesn't know the first thing about investing. If your company's Administration Costs + Costs of Revenue exceed your gross profit, the company isn't viable.

That is a very basic, straightforward call to make. If you wanna sell something, it costs stuff to make it (cost of revenue) and you have to pay people to sell it as well as do payroll and such (administration). This does not even consider product development, which is listed as R&D. Which is why i always use it as a measuring stick of whether or not a company is even viable to begin with. Even if they cut all research to a minimum and coast on previously developed technology - they're not viable. It might be a different story if it happens for a single year, but not if it's structural.

At the very least, this company is facing a very costly reorganization to straighten these costs out.

But, this brings us to a mystery. Why would the market cap, and thus the share price, be so high of a company that's completely not viable, and seems to bleed money faster and faster? There's more statistics than just market cap, and even those say there's undervalue now (while not before):

Enterprise value is Market cap plus debt minus cash, and is a slightly more strict measure of price. Price to book compares the current price to the book value, which is the dollar price of everything on the books. That's closer to the actual value of the company, but as i said before, the books can be cooked. Which is why i usually also look at the book value per share on seeking alpha, which doesn't actually list the book value per share in the overview. It lists the tangible book value per share.

The difference between book value per share and Tangible book value per share being, it excludes everything the company lists under "intangible" - stuff like brands that can't easily be accurately valued. As one might expect, there's alot of shenanigans that can be employed in categories that are admittedly hard to value, so i like the tangible number as a filter against that. As a bonus it also tells me quickly how much a junior miner has diluted so far, and considering they all generally have the same startup time, it tells me (at a glance) how far along it is in its development.

And here we spot a problem.

MINUS $2.59... isn't good. This means the current price of the shares is so high, if you sold the entire company, the shareholders would have to pay $2,59 a share to get full value back. Obviously, that means the shareholders are in for a guaranteed haircut upon liquidation.

Now, i've seen this before, especially with REITs or Banks that have alot of obligations/leases, so it doesn't immediately scare me off. But it is very noticeable for a company supposedly worth ~$15,5 billion (and that used to be alot more). At the very least, it tells me exactly where to look. As i said before, companies report alot of data, and the balance sheet is no exception.

We need to look at a company's assets. The stuff they say they own on paper. And as the above number reveals - and the title of the article gives away - it's not going to be hard to spot the problem here.

Out of $17,65 billion in assets, $14,47 billion is listed as Goodwill. This is a whopping 82% of total assets!

OK... ok... now, don't panic... don't panic. Surely the company must have a good reason for this right? Let's look at what the definition of goodwill in investing is to get a better grip on the situation (from Investopedia):

....Well that sounds almost too easy to hide stuff under. So let me get this straight:

Teladoc in 2020, a $3,4 billion company in assets at the time (consisting of ~$1,2 billion in cash, $1,7 billion in goodwill and 400 million in intangibles mind you), managed to buy a company with technology or a brand so valuable, it upgraded their valuation FIVE TIMES overnight?

You're telling me, that this company which has NET property, plant and equipment still listed as $75 MILLION, somehow possesses tech worth $14,47 BILLION?

Hell to the no. The $2 billion in "other intangibles" is fishy enough, but considering their consistently large (and growing) cash pile, there's always a chance they actually bought/developed that tech. Their R&D expenses are listed as $336 million (versus $75 million in net property and equipment that's equally crazy BTW) so it's not impossible. But $14,47 billion?

No way in hell. Especially not since their Cashflow statements show they made cash acquisitions worth $567,4 million and issued debt worth $1,1 billion in 2020, the year their goodwill shot through the roof.

Considering the ~$13,75 billion jump in goodwill, whatever they bought, they listed as being 9 TIMES more valuable than what they paid for it on a cash basis. And that's only if the debt money went straight to the purchase, since the year after, their cash pile grew.

In short - they're conning things. There's no actual tech there, it's simply a cash-pile for a company that buys things at grossly inflated prices to convince even more investors to give them cash. Not quite a Ponzi scheme, but close enough. Though it's going to get even worse.

None of their companies are properly integrated, because if they were, revenue and selling costs wouldn't already exceed operational profit. Reading through the latest 10-Q it seems the acquisitions were made with an already-inflated market cap, so it could very well be they're effectively scamming shareholders of other companies by first inflating their own stock value, and then offering a much smaller slice of a significantly overvalued company in the acquisition to buy things "on the cheap".

Their 10-Q mentions they bought InTouch on July 1st 2020 for a total of $1,069 billion, of which 4,6 million shares in common stock worth $903,3 million at the time at a share price of ~$196.37. Meanwhile, their quarterlies list their total assets in their September 2020 quarterly as $3,45 billion - and half of that was already goodwill.

In September 2020, their asset breakdown was:

$1,187 million in CASH

$1,364.3 million in total assets minus goodwill and other intangibles.

$2,078 million goodwill and other intangibles.

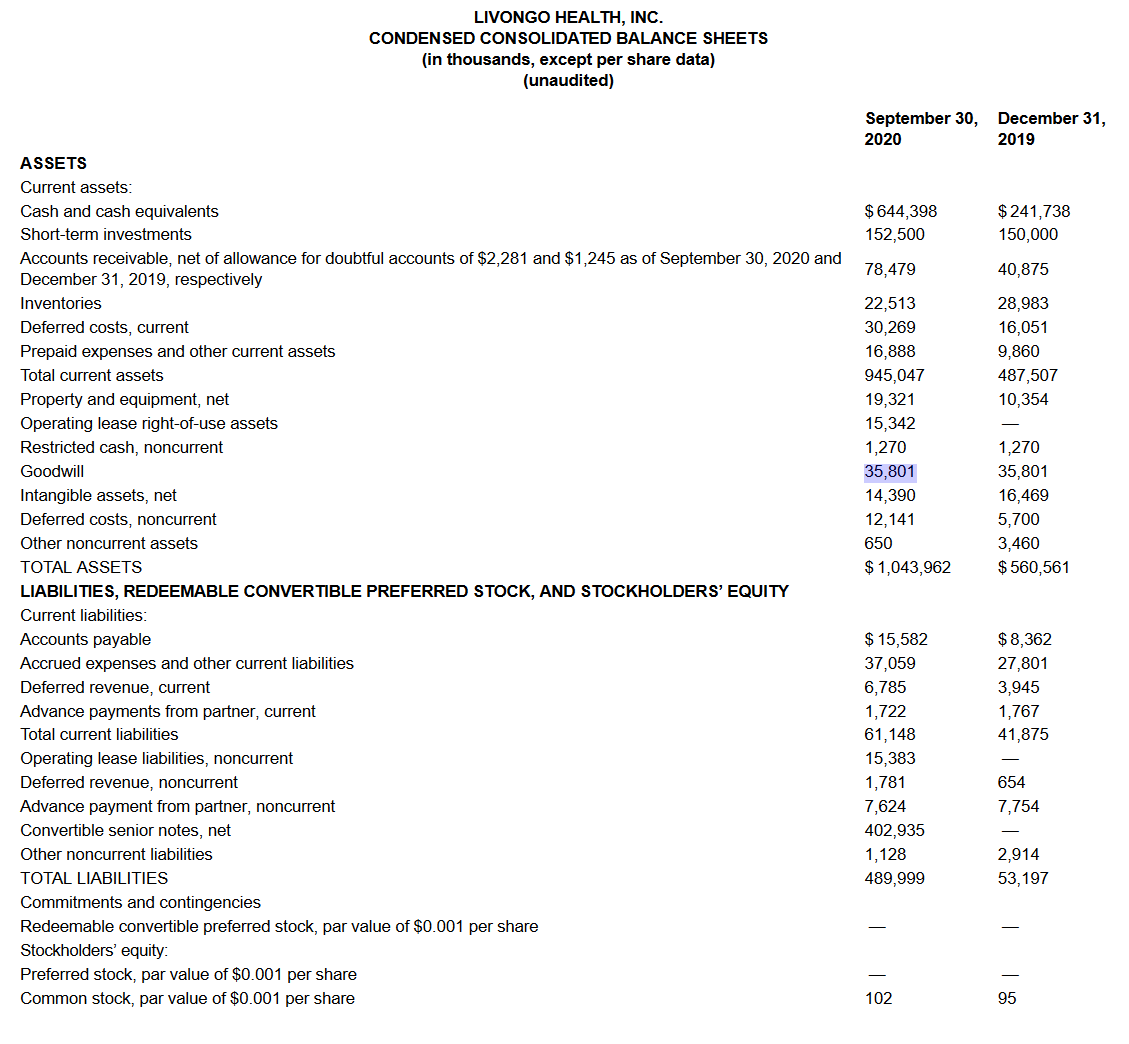

In that state, they merged with Livongo in late October 2020 - which last reported only 2 days before the acquisition was completed, a quarterly revenue of $106 million, versus 1 year ago revenues of $42 million - and at the time, Livongo had a $14,19 billion dollar market cap at last listing, while they listed a total assets of $1 billion, of which $35,8 million was goodwill (had to dig this quarterly out) and $664 million was cash:

So i can already tell you what happened. Teladoc themselves bought a lemon and waaaayyy overpaid for it. The con-men got conned. And instead of admit that they're a goner, they stuffed the entire company under "goodwill" to inflate their value and hide the damage.

And when i say way overpaid, i do mean way overpaid:

Honestly this is such an egregious amount compared to what was actually on the books of Livongo, i half suspect this was a "exit scam" orchestrated by some third party connected to both companies, and have the Teladoc shareholders pay for it (meaning Ark and idiot retail/institutional investors). Not only did the shareholders of Livongo get $13 billion worth of shares for a $1 billion company (possibly two on revenue growth), they also basically paid out the cash pile they already had, which made up 64% of their assets, in a special cash dividend.

This might be one of the biggest straight up heists of shareholder money i've ever seen. This isn't a Ponzi this is just highway robbery. I don't know who screwed who here, so i'm not making any specific allegations (the courts can sort everyone out, not my job), but it should be obvious this is about as fishy and above water as your average deep sea trench.

Now, if it was just this one company, i would've written it off as an anomaly of Cathie Wood being seemingly able to find scams (and invest in them) without fail, and i would've simply enjoyed watching the downfall (with my twitter thread to prove i was on the right side of history on this one). But i came across the same problem in another unrelated company while analyzing balance sheets on stream (though not as egregious), leading me to believe this happens far more often than i thought. I was asked about a Pot stock called "Tilray Inc.", and this is what i found:

Sure bud. A company with a $4,24 billion market cap, has $4,31 billion worth of "Goodwill and Other Intangibles". A pot stock? No brand is worth that much yet. That market is still very much in flux and in need of consolidation after the reddit based squeezes of this year. Compare that to another (random) company i looked up, called Green Thumb Industries (found via the "Peers" tab on seeking alpha), currently listed as a $4,49 billion market cap company:

This company isn't "worth" anything more or less than the last one. They have a little less net assets, true, but at the same time they report $827 million revenue, while Tilray reports $563 million - while their total operating expenses are very similar, $256 million for Green Thumb and $244.7 million for Tilray.

And this shows in their tangible book values. For the healthier Green Thumb:

And the worse off Tilray:

Now, IMO both companies are overvalued at many multiples tangible book value per share compared to share price. I prefer it to be more like 2x/3x maximum when looking for undervalue - though it's again just one statistic and there might be more in play. But just as it can indicate undervalue, it can indicate overvalue.

I would never buy a stock priced at $9.61 with only $0.02 of value in it. Granted, $21.52 > $1.31 is still insane.... but not unlike other overvalued stock i've come across in this insane market. And this is reflected in the shares outstanding: Tilray has diluted far more over its history than Green Thumb has. GT still has a chance to atleast grow into its market cap, where its tangible book value is still growing year over year. Whatever Tilray bought with its dilution and debt expansion - they're gonna choke on it.

They're already less competitive than similar priced stock. They're generating less revenue with more equipment. Acquisitions are treated these days like a surefire way to grow, but that's only true if you can integrate the new company successfully. If you can't clear the overhead of two separate company administrations (or more such as in the case of Teladoc), you're basically just bogging your company down with administrative supply chain issues. And servicing the debt load of your acquisitions could seriously hamper growth if the company you bought isn't growing explosively, or stops doing so because of the introduction of corporate culture (or in the case of Livongo, you're the fool holding the bag after the scam exits and you find out there's basically nothing there after the ink is dry).

I've had a look through other pot peers of the same size as Tilray, and some others have excessive goodwill too while others do not, including the second pot stock i looked at after Tilray of which a follower assumed it might've pulled the same trick. While i don't think it's a problem systemic throughout the entire market - i do think it's a low-hanging fruit way of cooking the books and thus often employed; low hanging enough that regulators should create stricter regulations for goodwill and what can be counted under it (and how) going forward, and for "intangibles" as well. Letting companies like this get away with it just hurts the confidence in the market in the long run.

While that pretty much concludes the investigation into goodwill, i promised to show a few more companies on Cathie's list that exemplify how she has no idea what she's investing in, and is only looking at revenue increases - as well as using her multiple actively managed ETFs to artificially pump up stock prices, which i'm pretty sure if it isn't illegal, it should be.

The other company that exemplifies Cathie's behavior of investing into overpriced cash piles would be UIPath, ticker $PATH. And Cathie Wood owns this company in SIX of her ETFs. Or atleast did on October 27th.

This company hasn't done as badly as the others since October, only being down to a shareprice of $47.71 - but that just means that this company has much further to fall later. Since you should be familiar with balance sheet stats now, lets first look at the overview of the company.

Aside from the insane Price/Cash flow, the price to book also stands out as being excessive. Generally i'd already consider a 6x P/B valuation (right now) as being frothy, with 1 or below being undervalued. As the April Twitter thread already showed, Cathie's not afraid of pushing stock to extreme values as a high price to book was more common than uncommon back then.

But other than that, it's not immediately clear if there's anything wrong with this company. Tangible Book value per share at $3.56 is low again compared to the share price, but this isn't unusual for overvalued companies. There's still a chance it'll grow into it, albeit slim. So why do i mention it?

Well. It's again when you look at the assets on the balance sheet that the problem becomes (or should become) clear immediately:

There's nothing there. The company's a cash pile, and nothing more.

Even if you'd assume goodwill and intangibles are all on the level and filled with technology/brand value (unlikely when the company's not even 3 years old), their actual, productive assets amount to $105.1 million.

Even if you'd lump everything under "long term assets" together as "productive"; their actual, value producing assets amount to 8,05% of ALL their assets!

The rest is cash!

The market cap is listed as $23,19 billion! When 92% of their $2,35 billion in assets is cash!

Whatever they plan to do with that cash you can't know upfront. There's definitely no deals to be found in this extremely frothy market. I've already gone through how Teladoc had to cook the books after buying a lemon. And naturally it gets worse.

Because Math. Cathie Wood owns 23,52 (rounded) million shares of this company across all her ETFs. Since it's public knowledge how much shares a company has outstanding, we can check this. For UIPath, it's 513.54 million shares in total (fully diluted).

23.52 million out of 513.54 million = 4,58% of all shares. Meaning Cathie Wood owns 4,58% of this company.

Since this company is 92% cash and that cash pile is $2,15 billion big, and Cathie Wood owns (and lets say spent for dramatic effect because tracking that down over time would be hell) $1,2 billion worth of shares of this company;

Cathie Wood spent $1,2 billion in cash to own $158,24 million in cash. Whatever the company will be in the future - that's the situation now, and has been for some time.

That's the competency of the "poster child" of investing of the current generation. Somebody who got endless press time and got talked up on all the mainstream channels. And it's not a fluke either.

Twilio: $1B owned across 3 ETFs. 4.27 Price to book with a $44 billion market cap valuation.

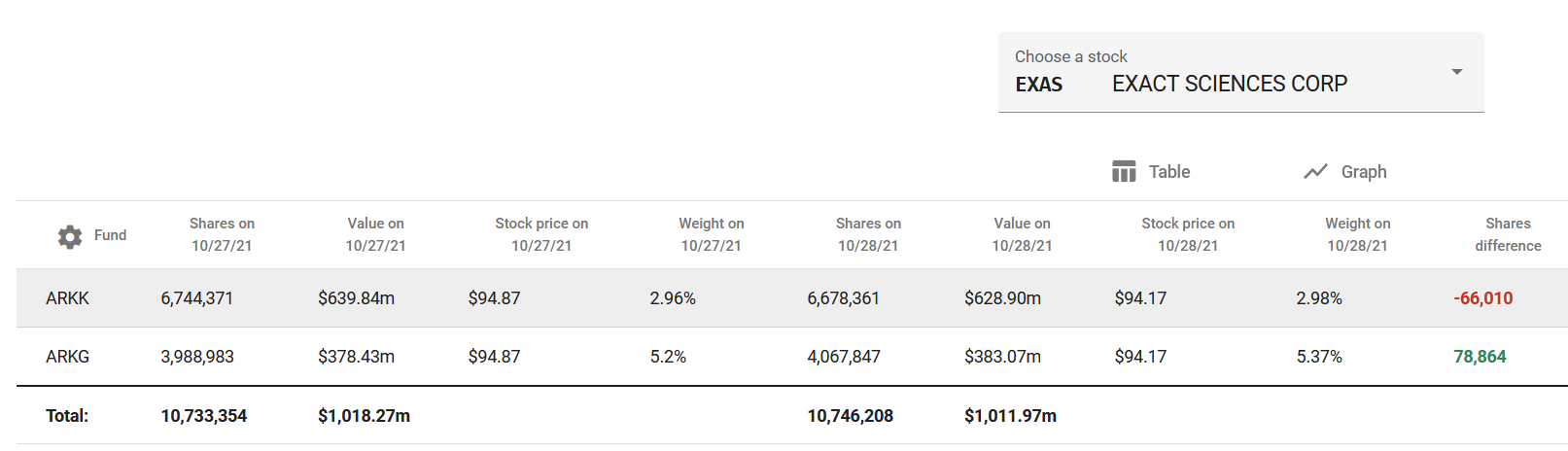

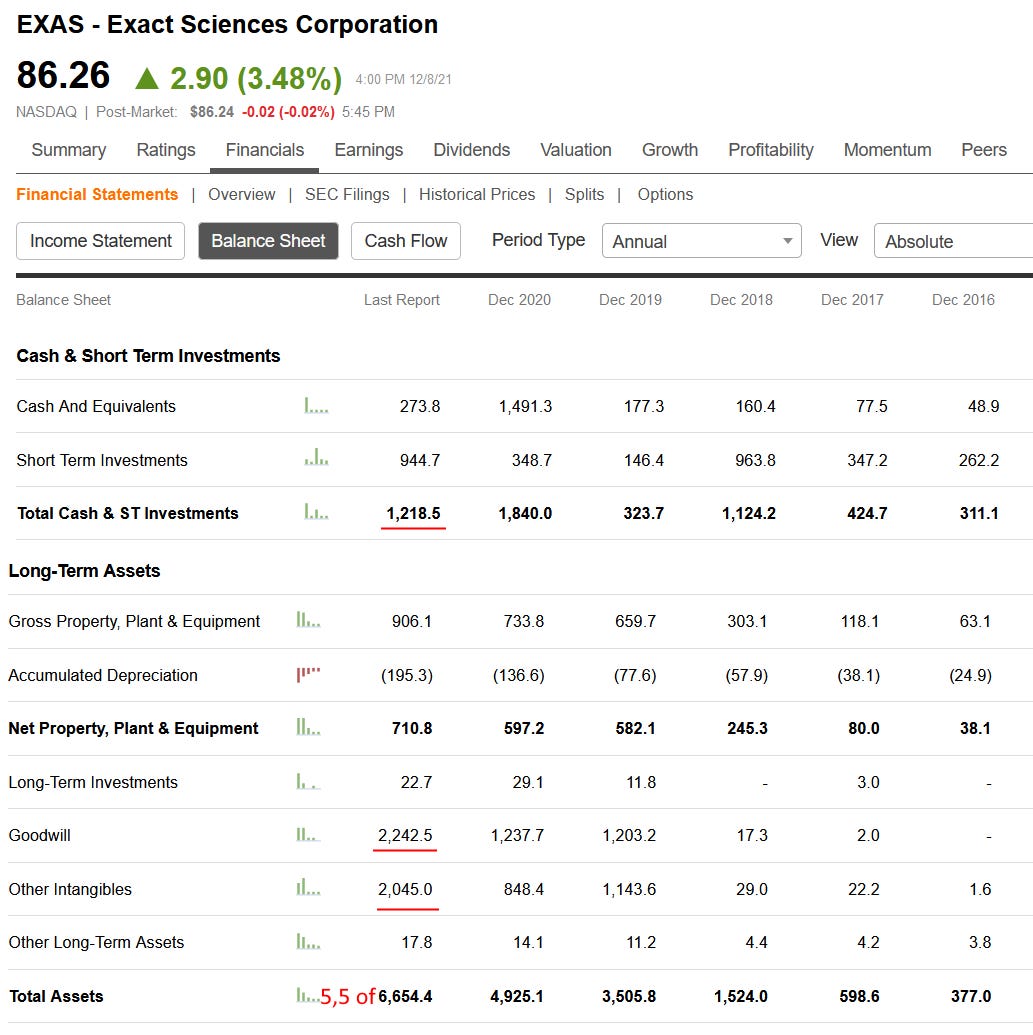

Exact Sciences Corporation: $14 Billion market cap, 4.15 price to book ratio. Tangible book value per share currently is $-4.82.

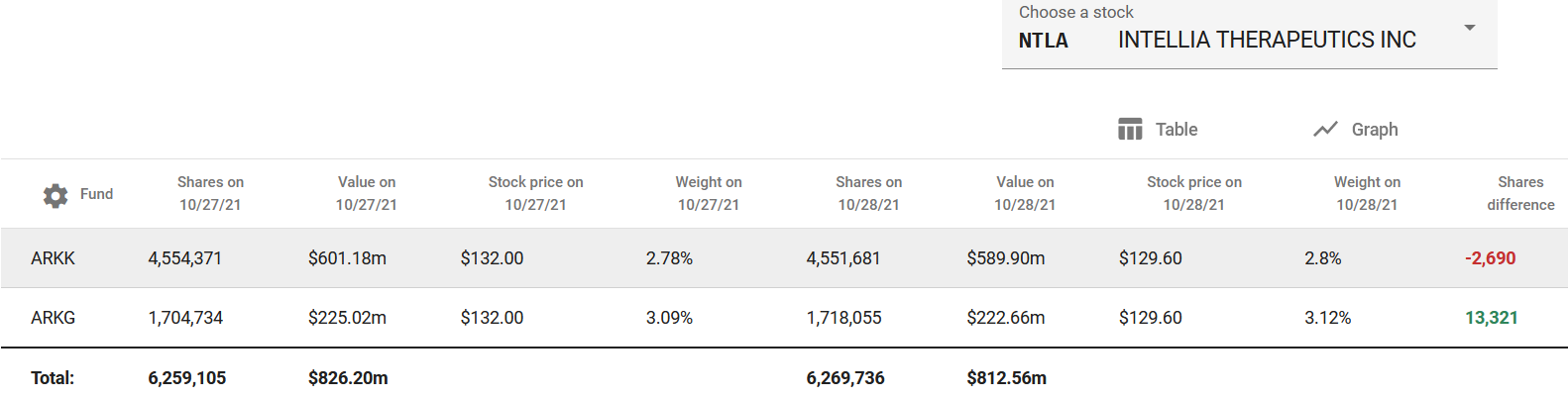

And Intellia Therapeutics. $7,5 billion market cap, 7.86 Price to book ratio. Tangible book value per share? $14.89.

There's actually so little diversity in assets in that last one they fit entirely on 1 page without scrolling! And it's not hard to find these companies either yknow, i literally just clicked on 3 random names in ARKK i never heard of outside of ARKK - at the bottom of the list even where the supposedly valuable stuff is.

Well, atleast these guys put some of the money to work, right? Atleast it's not goodwill again.

Regardless it's clear. All these companies show stellar revenue and revenue growth; because all of these companies have been growing cash piles in order to "buy their way to prosperity", and just acquisition whatever they need to realize these absurd valuations. Or they're just straight up incredibly risky biotech bets, made even riskier by pushing them to these valuations before the trials are done and the company hasn't even been tested by the market yet.

Even if the companies could realize their insane valuations, that realization is already priced in at this point! How are they going to grow from here?

If the price to book of a cash pile company is 4, then they have to find something on sale 75% off in order to realize that value! Since cash is all they have, they need to buy all the value to justify that valuation, and they can't buy value with cash 1 to 1. The only deals where you can 'supposedly' realize that sort of gains are lemons like the one Teladoc bought. Other cash pile companies looking to exit themselves.

Because that's how it works at the top of bull markets, and doubly so in manias. EVERYTHING is overvalued! You can't find deals to ride to the top anymore, even while everybody else still thinks their thing is the next big thing.

But honestly, Cathie is indeed the poster child of companies that think they can, because they don't understand a damned thing about actual investing. They run off the back of "mathematical models", which are nothing but garbage factories: Garbage in, Garbage out. It's a saying within computer science that's supposed to remind you that the model is only as good as the data you feed into it. And i'm dead sure at this point the only numbers going into Cathie's models is revenue growth. Explosive revenue growth = buy. Revenue slows = sell.

And never look at the balance sheet. As long as you don't look at the balance sheet, it's both valuable and worthless, and you can keep floating in the air like Wile E. Coyote refusing to look at the ground. As long as you can keep that up, you can keep looking in the mirror and tell yourself you’re a genius.

But then again, in a bull market, everyone is.

- Kirian "Deso" van Hest.

Find me on Twitter! https://twitter.com/DesoGames

Twitch: https://www.twitch.tv/desogames

My own website: https://www.desogames.com/

And buy my Ebooks for alot more content like this!

The Definition of Money: http://books2read.com/u/bzdaVz

The Definitions of Value: http://books2read.com/u/3yaZWv

Ethereal Value and the Cryptofuture: http://books2read.com/u/bMwrNA

Can we also point out that there is nothing proprietary about Teledoc. They are an online exchange, linking doctors to patients.

Awesome! What do you think of a company like NVDA.? Price to book is a whooping 33!