The Biggest Short: We're All Fucked.

The Biggest Short: We're All Fucked.

Data showing the collapse of financial "asset backed security" collateral, leading to the biggest short possible: Shorting the western financial system in its entirety.

First off, i must apologize for my absence in writing. Aside from being stressed to the max in my own endeavors, and going through a relapse of long-covid symptoms affecting my health and memory; while there has been plenty to write about since the start of the Russian invasion of the Ukraine, the ever-changing situation hasn't lent itself well to my usual long form articles. I've been very active on Twitter cataloging the various effects of the ongoing conflict on the financial system, while doing a few videos for more indepth looks at the various failing components of the global economy.

But most of all, i've felt dismayed to write anything, as most of the things that have occurred over the past quarter or two are things i've already written about in the past - and none of them good. While it's nice to be right, i can assure you, it doesn't feel good to be right about calamity. I'll take my solace in the people i managed to get out of the way of the steamroller in time. In any case, this article will also kind of serve as a recollection of the things i've written about over the years, now coming to pass.

Let's start with how the situation is in the markets currently. As i'm writing this (during the first draft), it has been a few days since Jerome Powell announced to the world rates were going up with 0.5%; but the economy was strong, there was no sign of a recession, and the negative GDP print in the first quarter could be explained away by inventory buildup.

The next day, the US productivity report proved him horribly wrong, coming in at -7,5% and the lowest reading since 1947. This while costs of production were up 11,6%. Both readings exceeded consensus by a wide margin. The data couldn't be more clear: Companies on the whole are not capable of raising prices or wages to keep up with inflation. While earnings might be continuous, contract negotiations and price increases happen only every so often, and inflation is continuous as well, explaining the lag.

This might seem counterintuitive to a generation or two brainwashed to think that prices lead to inflation, but this isn't so. Prices can cause inflation or speed it up, but only if the monetary base is there to begin with to afford the higher prices. Otherwise, it leads to demand destruction. And this small difference has Jerome Powell - as well as everybody else at all central banks in the world - completely confused.

If you want the full indepth explanation, you're gonna have to buy my first book, The Definition of Money:

https://books2read.com/u/bzdaVz

Which is the first part of a trilogy specifically written to counter the confusion sown over the years about the nature of money, and naturally, inflation gets its own chapter. I'll summarize it here.

Inflation (and deflation, which is exactly the same only the inverse), comes in 3 different forms:

Currency inflation.

Price inflation.

Value inflation.

Currency inflation deals with the amount of money available in an economy. This is the simple question of "how many dollars are there". If the answer is "more than before", you have inflation. It really is THAT simple.

However, the confusion is over what money is and is used for. Money is both used for trade as well as to store value. In this case, it suffices to think of "value" as "labor value". I.E. time you spent doing something of economic value, for which you were compensated at the time, and that labor can now be transported through time in the form of currency; rather than having to input even more labor at a later time.

This leads to 2 different concepts within currency: Money Stock and Liquidity. Money stock means "the total amount of money available". Liquidity means "the total amount of money available for trade at this time". The difference between the two is what we call "Savings", or what economists might sometimes refer to as "dead money", as it is money, but it's unmoving.

To make it as simple as possible; the answer to the question of: "If you print a trillion dollars, but never move it from the account you printed it into, does it cause inflation?"; is No. ONLY when that money moves from that account and starts circulating (meaning moving from person to person) within the general economy, does it start to cause inflation.

HOWEVER, if you print that money into an account which has no limit on moving the money, the money will be moved. Somehow, through some mechanic, it will be used. This is because money has "universal utility value", meaning it's useful to all of us, all the time. Money that we can't touch, has no value to us, but if we can, it has all the value.

Savings don't work any different, regardless of who has them. If we can't touch the savings, they won't move. That used to be partially done by "lock your savings up for X years to get X%!" which i remember from the 90's and 00's, before rates went so low as to make that proposition too unattractive. But that also happens naturally, through the very concept of "savings". That's not spending money, that's rainy day money... But still money.

That goes for everyone, and that's very important to understand. That goes for you and me.... but also Warren Buffett and his $150 billion cash pile.

Well, maybe a bit less now. I've talked this over with people in private chats many times, that eventually inflation would force Warren Buffett to deploy his capital, whether he found "good deals" or not, purely out of fiduciary duty to his shareholders. The reason he didn't before in 2021 is because his cash pile was growing as fast as inflation was. This doesn't count for everyone, but hey, it's Warren we're talking about here. For him though, that cash pile growth is reliant on the earnings of the companies Berkshire Hathaway owns.

Here we get into the 2nd type of inflation, and the one almost exclusively focused on by modern economists (while the few contrarians out there plainly say "it doesn't exist", which isn't true either); Price Inflation. And the logic is very simple: If you have a $1 apple, that now costs $1.5, then you need to find 50 cents more somehow; or you're not getting an apple; leading to demands for more currency.

That's 100% completely true. If prices of apples move up for whatever reason, such as a shortage of apples leading to fewer apples produced, then naturally people will demand more currency in order to afford said higher prices (while all other prices of necessary expenditures stay the same so income can't relocate). Yes, if people can't afford the higher prices, they're "priced out of the market" (meaning they won't buy the apple) leading to "demand destruction" (if they can't afford apples, they will no longer buy apples, no matter how many people "they" encompasses). This has nothing to do with what people want anymore, they simply can't afford the apple, so they're not getting the apple.

But if they CAN afford higher prices, they WILL afford higher prices, as nobody likes "being priced out of the market" on necessities such as food. Now sure, we might be able to miss apples if we have substitutes for food - but if apples is all you eat, "being priced out of the market" means starvation, and you WILL pay WHATEVER to not have that happen.

And this is why you need both Currency AND Price inflation to make sense of the whole thing, because if people have the savings (or any other access to more money) to afford the higher prices, liquidity increases, and prices are based on liquidity, not money stock (AKA dead money); as that's money not available to the people trading apples, so it has no value to the people trading apples, therefore it's not included in the price.

To simplify, the cost of pears isn't included in the price of apples, as people demanding pears aren't demanding apples with the same money - and money can only be spent once. If they want apples as well, then they need more money to afford a different product.

Which immediately shows how the central banks ignoring currency inflation for so long has been a catastrophic mistake. I don't even need to change anything in the above explanation to explain that.

I just need to capitalize apple to Apple.

And here i can give a callback to the first article i wrote: QE is inflationary and i have the charts to prove it:

https://www.desogames.com/qe-is-inflationary-and-i-have-the-charts-to-prove-it/

The reason why "there wasn't any inflation" between 2008 and 2020, why central banks were stuck below a 2% CPI for a decade, is exactly because of my above explanation. If you print money into one account and never move it, it doesn't cause inflation.

But we can widen the scope of that definition a little bit. If you print money into 2 accounts but never move it, is there still the same lack of inflation? Yes. And that stays Yes for higher numbers too. So clearly, movement is the key here. Which also means money stock can go as high as it wants; as long as liquidity stays muted, inflation does not happen.

In the assets the liquidity stays muted in.

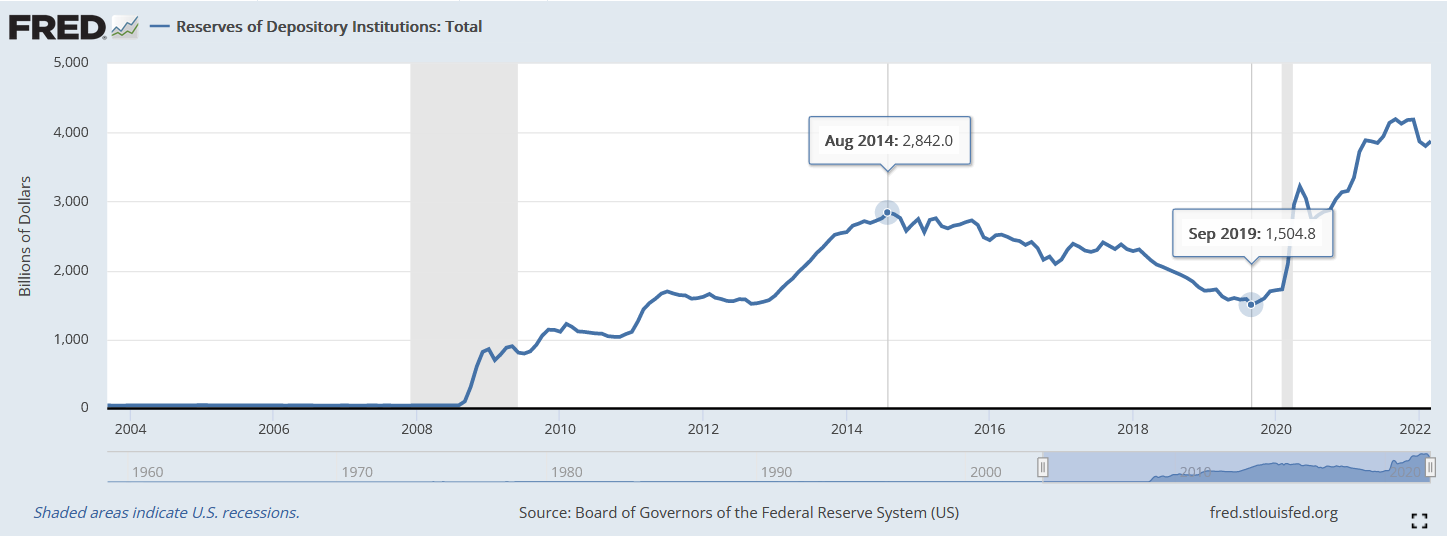

After 2008, QE ended up on the banks balance sheets as "excess reserves". This was effectively printing money into an account with heavy restrictions on what they could do with it. Partially through offering a yield on it (more free money! who says the dollar's not a Ponzi), partially simply by decree from the Federal Reserve. That money didn't move, so it couldn't cause inflation in the general economy, but it's still money.

Money on the balance sheet of banks. And as such, can function as collateral.

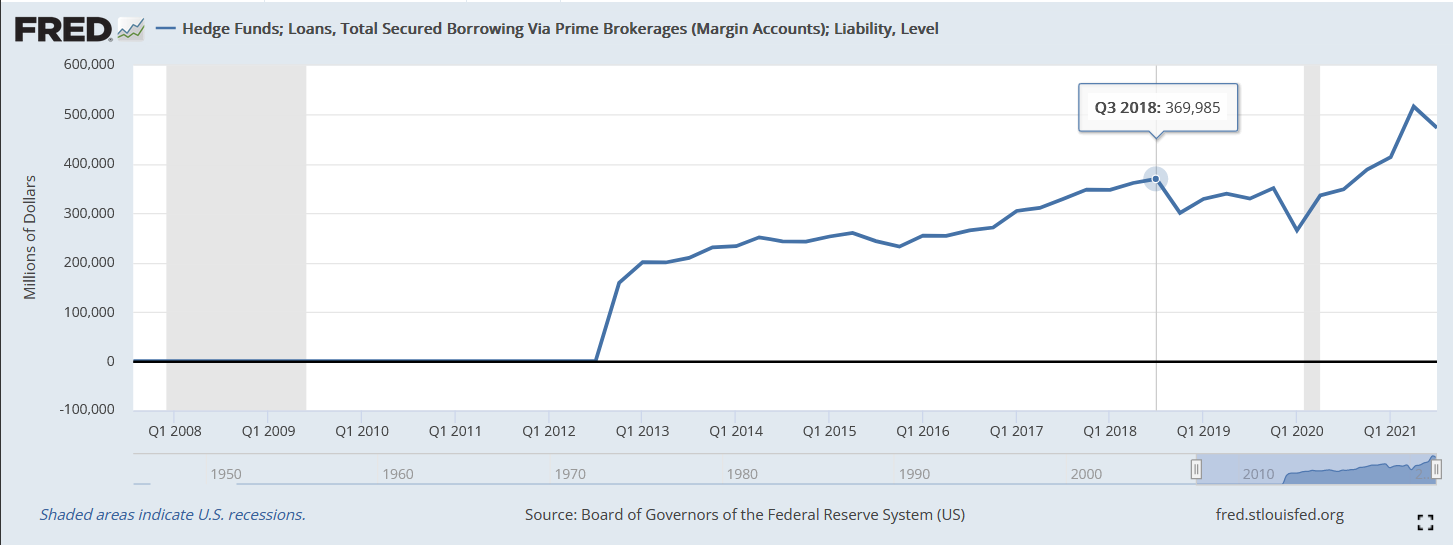

The "excess reserves" data got discontinued in 2020, and it's all just "total reserves" now. I'm not sure if that means that money is officially circulating within the real economy or not, but the inflation numbers sure would indicate it is. The 2014 top is denoted by the end of QE, and the 2019 bottom by the restart of QE. Hedgefunds loans took a dip when the late-2018 crash happened, and rates were cut to prevent the system from deleveraging too much, yet again.

Regardless, at this point in history it's not hard to see where the money ended up. Because Margin accounts are loans specifically made to be put into the stock market, the banks lent it out to hedge funds if not their own prop trading desks, and it mostly all flowed into the stock and bond markets, where it has stayed due to the nature of margin and credit. Also, when the NASDAQ goes up 10 TIMES between 2009 and 2021, that offers a nice incentive to keep your money put. I'm pretty sure those are Ponzi-level risk-free returns, too.

But not just the stock market. The same trick has been played on synthetic markets, like corporate debt. This has allowed companies to stay afloat longer than they should've, by paying down previous debt with new debt. The money from the debt that is paid down gets levered down again, with only the interest remaining as new money available to the real economy - which is the "inflation" that was measured over the past decade. Bond coupons, company dividends; new income. It wasn't the real inflation number as measured by currency inflation, it was the "leak" coming out of the synthetic markets causing price inflation, which was then measured after the fact.

That doesn't count share buybacks, as that keeps the profits virtual - the share price moves up, which is a meaningless number until you buy or sell. This is very visible in all the major companies, where Apple, even with $100 BILLION IN PROFIT, only offers a 0.58% dividend. Which means that, if you buy in now and the share price goes sideways, you'll get $58 a year for every $10,000 you put in originally. How could you ever get to 2% inflation that way?! Not to mention that comes out of earnings, so it's recycled inflation, rather than new money directly.

The same process is also how inflation hurts the poor (and the unborn). Yes, assets increase in price, but if you don't have assets yet, you're stuck buying them at the higher price now. And the poor have the least amount of durable assets and the most need as a slice of their income for consumable assets. People who bought Apple in 2009 are up 2000%. That means $10,000 invested in 2009 turned into $200,000. Which also means those people are now receiving $1,160 in dividends each year from their $10,000 Apple shares purchase, while the person investing $10,000 today only gets $58 each year, at the same percentage of dividends.

I've said before, if we paid in stores with Tesla shares instead of Dollars, we would've been talking about hyperinflation ages ago. Because, as those shares went up in price, so too would've the price of groceries. As more money becomes available, the prices are raised as otherwise supply is emptied out over and over again until they are, through supply and demand mechanics. If everybody is rich, soon enough everybody will be poor.

Add to that Crypto, which has served as a lightning rod for fiat currency, and with its many Ponzi schemes has actually served as a "liquidity sink" for generalized inflation, siphoning off real dollars from the commodity economy and providing literal digital tokens in return, with no guarantee what so ever dollars can be extracted from the ecosystem at a later date.

At the time of writing, Bitcoin isn't dead yet, but it seems to finally be dying. Here i can give a callback to my second article; why i hate Bitcoin and why Tether will end up killing it:

https://www.desogames.com/why-i-hate-bitcoin-and-why-tether-will-end-up-killing-it/

The summary here being that Tether's a Ponzi scheme without backing and Bitcoin will die through normal market consolidation mechanics; as it becomes unprofitable to mine and miners shut down, meaning the strongest and biggest survive, until eventually you have a few players or a single one which could easily collude to break Bitcoin's 50% rule, thus breaking security, trust, and the whole point of a decentralized trustless currency (even before the attack actually happens as people get skittish and sell out). Once it starts dropping, it won't be the people holding alot of dollars that'll be holding bags.

Though, i'll also throw in my 3rd book, Ethereal Value and the Cryptofuture as a reference for anybody wanting to understand the problems with Bitcoin's value proposition, and how to fix it, as there might be a future for crypto yet:

https://books2read.com/u/bMwrNA

To be sure though, i don't expect any of the main figureheads within crypto now to pick up on it or even to survive the mania, as they've all made right fools of themselves. This book is written for the next generation, so that when they return to the drawingboard they won't have to reinvent the wheel - i've already done so. In an ethical way that powers innovation directly by tying it to mathematical research (and turning Proof-of-just-Work into Proof-of-actual-Value that way); and made sure it stays free for future generations to use and implement by giving up the patent rights. If you want to approach crypto from a value perspective; this is the way forward.

Or yknow, you could follow the guy pumping his proprietary bags every other week rather than the person who cares about the truth only and tosses this kind of quality work out for free. The books cost just 1/1000th of 1 Bitcoin (for now).Your choice.

And coming around to this on the second draft a week later, this seems alot more prescient as crypto has since taken a nosedive due to Terra Luna, an algorithmic stablecoin, blowing up and taking many tens of billions of "value" with it. I had been warning about people about this before, even just 2 weeks before it happened (somewhere in this interview from about a month ago):

But i might as well run through it again since it's relevant to the topic. Terra Luna tried to keep the peg of its stablecoin UST by buying and selling a companion coin called LUNA according to "the laws of supply and demand", which i'll talk more about later. However, in their documentation, they only make mention of selling UST for LUNA and LUNA for UST, in order to contract and expand the supply of each. The idea being at the same level of demand, a lower supply means price increases while a higher supply means price decreases. Which is true.

But WHAT price?! Not once does their documentation mention dollar demand, which is what these things are priced in and linked to, considering UST was a stablecoin. That is a massive red flag. Because WHY would anyone WANT to hold a rapidly depreciating token?

Sure, buying UST by printing and selling LUNA in the open market raises the price of UST and lowers it of LUNA, but there are people holding LUNA. WHY would they continue to hold it when they KNOW the price is dropping and will drop further? The utility of the network here doesn't matter, as if the token dies, the network goes with it. Long term incentives don't matter if the network will die short term (looking at you, USDD).

The simple answer is the people won't hold. That's why the mechanism wasn't active until late in the crash, and the usual peg fluctuations were solved through open market arbitrage operations instead; which worked while LUNA was going up in price. The simple proof for that is in a picture i made of LUNA's circulating supply before it went crazy, and matched it up to the inverted market cap of UST. If these coins are linked, then UST should go up when LUNA goes down in supply, and the reverse should be true as well.

Clearly, the reverse isn't true. This effectively makes it a Ponzi, because the market cap of LUNA will be in no relation to the market cap of UST. As people noticed in the crash, if UST wanted to survive the bankrun, LUNA's market cap should've been alot higher than it was when everything fell down. Had it been higher, more dollars would've been gained per LUNA at the start of the crash, meaning it would've taken longer to reach the exponential phase, and the system might've even survived.

However. This would've required an action that was impossible for the system. As when the LUNA supply expands, the UST supply is supposed to contract, and where are you going to get those USTs? Algorithmic stablecoins assume arbitrage, but that doesn't have to happen if nobody wants to buy a depreciating asset. Why swap a stablecoin for a rapidly-losing-value-because-it's-being-printed coin?

Again, the answer is people won't. Hence that the supply of LUNA and the supply of UST were in absolutely no relation to eachother before the crash. I can't even explain where that large supply of LUNA that you see in the middle of the chart came from. As far as i know "it must've just been printed under some bullshit excuse".

As for what triggered the run and overwhelmed the normal market operations; that was a classic bankrun. Most USTs were being stored in an app called Anchor, which promised 20% returns on deposits - which is literally the average percentage offered by Ponzis. At its height, 14 billion out of 18 billion USTs were stored in there until something spooked the depositors. This was only inevitable, as the guaranteed 20% rate had been changed to a dynamic rate and started to drop; as 20% was unsustainable and how to deal with the "yield reserve" running out by early May was a lively discussion on the Anchor forums in March. As UST became less competitive with other Ponzi's in the market, eventually people would've cascaded towards the exits anyway.

Anchor dropped 2 billion+ in deposits really quickly and then continued to bleed more. Do Kwon, the infamous purveyor of the stablecoin, actually made matters worse by posting and misreading a chart comparing withdrawals to wallet accounts. Where he pointed out 68% had been drawn out by a single wallet as justification for an "attack" narrative (which some community members still believe), the correct shade of blue actually said "others", showing that 68% of the total was being withdrawn by the smallest of wallets instead of 1 big wallet, confirming a bankrun in progress himself and spooking everybody else to run for the exits as well. After that, the rate of decay in Anchor accelerated to a point where it lost a billion dollars worth of deposits every 4 hours, and nothing could've stopped it.

I made a twitter thread recently that goes deeper into the ponzinomics of the coin:

And we've since learned that the $1,5 billion worth of Bitcoin deployed during the crash to "stabilize" the coin were sold in just 2 transactions at near par for a nowhere-near enough amount of UST, clearly bailing out 2 large players and screwing over everybody else in the process. 80,000 were sold, 313 are left as the Luna Guard Foundation now holds a billion and a half of worthless UST. And Do Kwon wants to basically reboot the chain and airdrop new tokens to the old holders, to pay off his previous Ponzi with the next one.

I'm baffled regulators haven't raided his offices at this point and that this is allowed to continue. It's hard not to long for the days where these charlatans were simply dragged out of their homes and beaten in the streets. Clearly they have no shame and won't stop until somebody puts a stop to them, which the regulators just seem to refuse to do (again if the charlatans aren't outright protected by regulators. Looking at you, BaFin). Should they continue down this path, it will come down to beatings again.

For the final comment on Crypto, considering Tether depegged in the same event as LUNA started taking the Bitcoin price down and still hasn't repegged after 5 days, it means there's more trouble on the way. Tether lost $9 billion in market cap, which should be just about all the cash they declared in their attestations, meaning actual dollar liquidity is pretty tight right now. The same that counted for LUNA, counts for Bitcoin and Tether: Why would you hold a fastly depreciating asset?

And while Bitcoin might have a fixed supply, it does not have fixed liquidity. Infact, it's culture within the Bitcoin community to "HODL", and the vast majority of retail actually does. Meaning, Bitcoin Liquidity is only a fraction of the true supply of Bitcoin already available, and price reflects liquidity, not supply (or money stock, which is total supply of money). It's hard to pin a number to it, but i have seen articles come by saying only 5% to 10% of all Bitcoin is actively traded, and the rest held.

Coiners use it as proof that people want to hold this asset and the price will go "to the moon", but everytime i see it pass by all i can see is "the price will crash once those people do decide to sell". Once the outsized returns of Bitcoin turn out a fraud (we're close to that i feel), it'll go. If Tether fails its peg and people panic, it'll go. There'll be "a bankrun on Bitcoin" as cold wallets turn hot, lots of new supply hits the market at exactly the time nobody wants to buy it, and prices crater. 4 billion out of 18 billion UST meant the UST liquidity at that time was 22% of the money stock. For Bitcoin it's definitely lower than that. And that's even without Tether failing, which'll show that alot of "dollar demand" wasn't actually dollar demand, but Tether-demand, previously considered as good as a dollar.

Needless to say, i've been advising people to stay the fuck away from crypto for a very long time now. I'm not a no-coiner, i believe in the parts of the technology that work, but not that the current iteration doesn't have many flaws. I'll leave the synthetic markets with the comment that crypto does have a bright future in my opinion, but it needs another decade in the oven atleast. If not in the least to weed out the current con-men and build a new space around value as a basis. Again, buy my 3rd book if you want to learn exactly how to do it considering i spent a decade thinking about the problem (and buy the first 2 books to understand what the hell you've built; Do Kwon sure could've used the lessons).

So, why is it that prices in the general economy are rising now while they weren't before? Well, because there's more things to invest in the markets in than tech companies, bonds or crypto. There's commodity companies as well, as well as commodities themselves. Wheat futures, Oil futures, oil companies. Productive stuff, that if invested in so demand expands at equal supply, will raise prices of goods consumers buy, as those goods use other goods as input costs. And futures markets are used as a pricing mechanism specifically to determine what the goods should cost.

For a long time though, there wasn't a problem. Non-financial companies basically run off the back of earnings (and cheap debt for zombie companies), and as long as the earnings don't increase, the companies don't look attractive VS companies where earnings do increase, and are expanding on the basis of cheap credit (revenue growth outpacing profit growth). The only way for commodity companies to increase their earnings is if they raise prices on their products, which can't happen if people don't spend more money on their products. It's sort of a vicious cycle that only expands production slowly as long as there aren't any shocks to the system such as supply deficits or influx of money.

How much the companies can expand is then determined by economic conditions; how easily can their average customer afford the higher prices? If they can't afford higher prices, you get demand destruction, and earnings stabilize again. Meanwhile, since the vast majority of commodities are bought by average people, who generally don't (or didn't) participate in the stock market, and have no additional income; prices and earnings are generally in equilibrium.

Since real wages haven't increased since the 2000's or longer, it's been really hard to create inflation in the general economy, since every commodity price increase has been met with an equal amount of demand destruction. This in turn has lead to portion sizes decreasing (shrinkflation) or the quality of products decreasing (stripflation) to compensate without raising protests about higher pricing, and increase earnings "without" causing price inflation.

But that process has an end. And that end we started with locking down the supply chains at the start of 2020. To be sure, it was always going to happen as the Repo crisis happened in 2019; but we sure as shit hastened the end by kicking the supply chains when they were already starting to become stretched, and the pandemic itself couldn't have come at a worse over-levered time for the financialized economy.

Now we have to talk more about supply and demand, and how it affects value. Though, again, if you want the long explanation; i've thought of that with book no.2, The Definitions of Value, which goes through everything that affects value and our perception of it:

https://books2read.com/u/3yaZWv

The gist here is simple. As long as one stays equal, but the other changes, prices move. So if you have the same supply, but larger demand, prices go up. Same supply, smaller demand, prices go down. Smaller supply, same demand, higher prices; bigger supply, same demand, lower prices.

It's demand that's poorly understood, as to modern economists it's merely a mathematical variable, and as such needs some sort of input to be calculated. While in actuality it arises from the wishes of the people owning currency, with desire being the root cause of demand. If they wish to buy something en-masse, it'll go up in price, regardless of actual value. No need to look further than NFTs in our modern day. If it has a price, and more than one person is willing to pay that price, it'll go up in price until we find the amount where only one buyer is left. Whether that happens by auction, or back-and-forth trading until it starts selling for an equal or lower price, hardly matters. This action's controlled by the 3rd type of inflation, value inflation, also described in my first book and rounding out the "inflation triangle" that covers everything inflation and deflation wise.

The key thing to understand about demand, is that demand comes before supply, always. This because demand can be hidden (a "gap in the market"), it can shift rapidly (NFT sales collapsing), and it's far more "elastic" than supply will ever be. People can demand gold faster than a new gold mine gets started, leading to rapid supply deficits where just weeks or days before, there weren't any at all. The semiconductor market during the pandemic is a perfect example of how a big event can shift demand from other sectors onto one all at the same time.

Since demand is fickle, we have to limit people from demanding whatever they want all the time. If everyone had access to unlimited money, what happened with NFTs over the past year wouldn't even begin to describe the asinine investments we'd make then. People have to be forced to make value judgements, and that is easily done by restricting the thing they demand all other things with: Money. If people don't have unlimited money, they can't have unlimited demands.

Except that in 2020, we first shut off supply by decreeing industry to shut down - and then gave everybody stimmy checks to actively prevent demand destruction from happening.

This is why i wrote a trilogy of books, instead of stuffing everything into the same book, as you get kind of a jumpy mess like this article is if you try to deal with money and value at the same time. It's all connected, but they are still each their separate things and should be separately understood before the full picture of the jigsaw puzzle makes sense. In my books i clearly describe the system behind it all - which is the only way to understand any of it (and charge for it cause that took a fuckton of effort). You need to understand both the differences between price and currency inflation, money stock and liquidity - but also the effects of supply and demand, which are expressed through currency.

It's why i need to explain inflation first before even getting to supply and demand, because if you don't understand that a large money stock allows liquidity to grow, rather than demand destruction to take place (and without thousands of words of explanation upfront, that sentence itself sounds like Japanese to people); then you can never understand why prices are exploding right now. Like the Federal Reserve couldn't and still considers it a mystery.

It's because the money to afford said prices was printed. Lack of production + lack of demand destruction = a draining of inventory, which is exactly what happened. That continues until either production comes back (it didn't as investment went into speculative assets which went up faster), demand destruction ends (which it can't if people jump into speculative assets which continue to increase in price which just multiplies their money), or the inventory is empty (reality says this one happens if the others don't).

When producer inventories are empty, they'll increase production to maximum (this is also causing the supply chain accidents all over the place, by producers running beyond capacity through compressing safety margins), which starts draining the raw resource inventories faster than before . When those inventories are empty, the next batch comes out of the ground whenever, and will be sold at auction: Highest bidder wins. Producers initially eat those costs by compressing profit margins as not all their customers are benefiting equally from the mania; until they have to raise prices, or go bust. When it's a choice of personal survival, they will raise prices, even if that makes life more difficult for everybody else.

For a more indepth look at supply chains specifically, i wrote another article called "The Chain of Supply", which dove deeper into overstretched supply chains, and highlighted one before it broke down to show the process in motion; "before" it happened:

Which has also since come true; the price of milk is now at an all time high while cheese is in the 3rd highest price spike ever, moving up. There have been quite a few games based completely around building, maintaining and upgrading logistics supply lines, and i played those for quite a while too.

That's one of the reasons i've been saying "this is an every man for himself situation, but most people don't realize it yet" for a while now. Everybody will take this action as it's in their personal benefit to do so, and detrimental if they don't. There is no stopping that. It's even got a name, called the Tragedy of the Commons. The following video (from 2017) explains it well within 10 minutes, though it needs to be added that self-interest isn't always a choice through external supply deficits:

Higher prices then fuel the demand for (more) money by the general public. Since the vast majority of income is earned through wages, wage demands increase (though the same goes for social security, increasing government costs, spending, and inflationary pressures if that money is new money, or tax pressure otherwise). Companies have no choice but to raise prices doubly so; once because of input costs, once because of labor costs.

Since this starts raising prices faster than wages (as people only have wage income, but companies have wage AND input costs), it causes a wage-price spiral, where higher prices lead to demands for higher wages, which cause higher prices leading to more demands for money. Note that this doesn't cause inflation directly if money isn't printed to met said demands, but since it does increase misery through demand destruction, money nearly always is printed to avoid said misery.

In early 2021, as this process started to run away and show up in the CPI, the Federal reserve came out and said it was "transitory" inflation. This because, again, if you only look at price inflation through supply and demand mechanics, it makes sense. Higher prices will continue until people cannot pay for the products anymore, which drops demand and allows supply to catch up; while the higher prices increase income which can be spent on expanding supply to bring said new supply online.

And it's the exact same reason i called bullshit right away, as it completely ignores money stock and liquidity. The large amount of money out there which further got added to during 2020 meant liquidity could increase, while the fundamental action of shutting down supply chains gave money a reason to move out of money stock and into liquidity. A real, unavoidable, non-financial reason. Products just got made less, so they had to cost more.

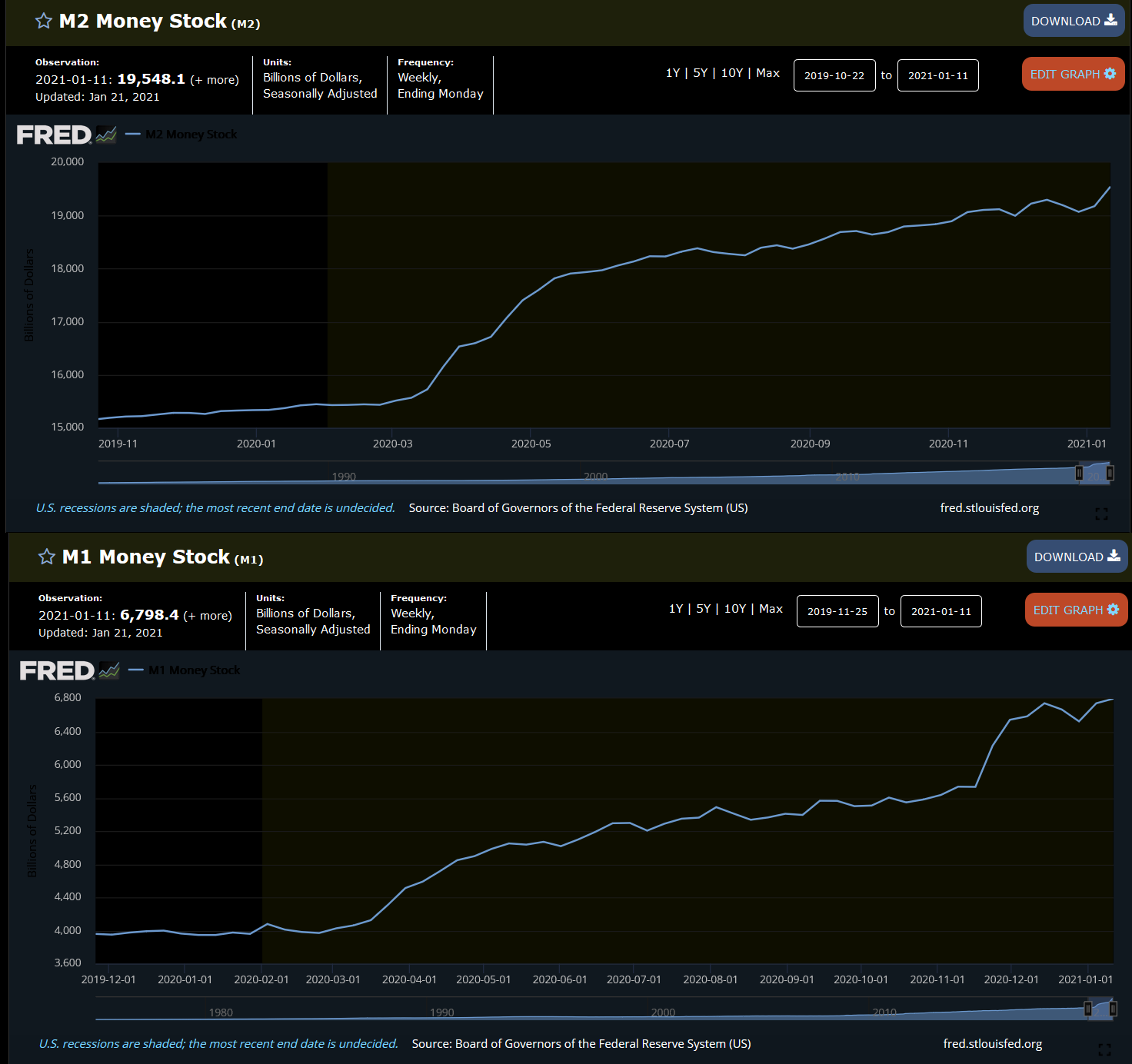

This is a screenshot i've often posted on Twitter, and one of the best reasons within this entire century to "make screenshots and document everything". It might be the most important screenshot i have, to answer the question "why is there so much misery". Not long after this screenshot, the Federal Reserve retroactively changed the M1 and M2 money stock measures, back to May 2020. They explained it as a technical change, as the main difference between savings and deposits used to be a lockup period that they removed in early 2020 to give people easier access to liquidity, basically making M1 and M2 indistinguishable (and unwittingly further opening the door to inflation).

Except that, with the retroactive change, we cannot see how much money has moved out of savings and into circulation. While we previously could. And the chart above clearly shows why: Around the November election, people took out a trillion of savings and put it into liquid accounts. This doesn't decrease M2 as M2 counts M1+savings - but it does show up as a spike in M1. Which is why M1 looks like M2 now. To hide the spike.

The same spike that killed the correlation in my QE article. If i have any evidence of Jerome Powell being actively malicious in his decisions, it's the changing of M1 into M1SL AFTER the above readout.

Only people who know they're guilty, hide their crimes. Having said that, i don't think he's lying out of malice or evil reasons, i think he's lying out of pure incompetency; that he's completely and utterly out of his depth (he's not even an economist, so no surprise there), knows things are bad, but has no idea how to deal with the situation or to get out of it; nor do any of his stooges. So he "wings it" on the policy while actively trying to sweep his mistakes under the rug, like anybody who's bluffing. Bravado, not confidence.

It's still criminal - but not evil. The reason people think it's evil is because it's more comfortable to think actually he's in control, he's just pretending to be stupid. Because then, atleast somebody is at the wheel; they just don't like you. It's better to have an evil man at the wheel with a sense of self preservation; than absolutely no one. Surely, even if he's corrupt, to save his political career he'll do the right thing... right?

This is another thing that i've written in more detail about before, in my article "Why inflation isn't going away":

Inflation can't go away when there's such a large money stock out there to flow into liquidity, allowing people to pay the higher prices and preventing demand destruction. Whether this is in cash or an unlimited ability to attract credit, doesn't matter in a debt based economy. Debt based dollars will be fungible with and indistinguishable from cash dollars, as it's all debt in the end anyway.

This will be true even when people's incomes are squeezed, as that doesn't stop them spending, it merely re-allocates their spending from discretionary to mandatory spending. Or put differently, just because people stop buying clothes, doesn't mean food prices are going to stop going up. That can only happen with an increase in supply, a decrease in demand, or a decrease in liquidity dropping prices overall. Conversely, if the liquidity stays available and increases, prices must increase at the same level of demand. Which for food is pretty constant.

Demand can be irrespective of number of people, as it depends on capital just as much as people. If raising prices from $100 to $200 means now 10 people can afford the product where at first 20 could, but the remaining 10 double their amount of purchases because they can afford to do so, then prices must continue to increase. Demand and supply stay equal even if people drop out, because the capital within the market continues to stay equal.

Prices aren't priced in people or number per person (until supplies become tight). They're priced in currency. Therefore, if the currency is available to drain supply, it will continue to do so as long as the desire to do so is there. This goes for goods that are in constant demand like food, but also discretionary goods with a constant supply. As long as the same amount of TVs get made and bought, and that demand lies higher than supply, prices continue to rise - to infinity if they're allowed to.

Hence, considering there's still so much liquidity out there that can flow into commodities, even if people are priced out of the market, not enough capital is. Berkshire bought $51 billion worth of stock in 1 quarter. $7 billion of which went to Occidental Petroleum, just 1 oil company. The entire Uranium sector is $30 billion. What would be a small allocation for Buffett, would be huge for the industry in its entirety.

As prices go up further, it once again becomes the fiduciary duty of asset managers everywhere to allocate more capital to commodities to protect themselves from price inflation. Since this increases prices further, it becomes a self-fulfilling prophecy that'll continue as long as capital is available in exponential amounts to continue to flow into commodities.

And people REALLY underestimate how much capital is available VS how much capital is located in commodities. This process need not end anytime soon once it truly gets started. And get started it must.

Which brings us to the title of the article, and the general theme: Collateral.

To shortly describe what collateral is; collateral is an asset that backs a loan. For example, a house is the collateral backing the mortgage on that house. Since a mortgage is a loan a bank extends to you for the purchase of the house, if you cannot return the money, you have to give up the house. This process works for every asset; if you've got a collateralized loan on silver, if you can't find cash to repay the loan, you have to give up the silver.

These are commodity based examples as they're simple to understand, but the same process also works with financial collateral. For example, if you slice up mortgages into mortgage backed securities, one of these so called MBS can be used as collateral for another loan, or even multiple MBS can be put into a CLO, which then serves as collateral itself. While the ultimate underlying collateral are still houses, because they've been fractionally sliced up, a MBS counts as a financial instrument. Since CLOs are slices of slices, we go as far to call these and similar things "derivatives", because their ultimate value is derived from financial instruments, rather than assets that actually exist in reality, as they are too far removed from them. The CLO market can bubble up and turn to shit without destroying a single house, as we've seen.

This example also gives a quick introduction on the alchemy of how real collateral can be turned into financial collateral, in the same sort of way homeopathy doesn't work. If you dilute anything enough, it ceases its original function, and becomes something else; usually something worthless. This goes for the bonds underlying the entire the Western financial system as well.

Which leads me into most of the collateral backing loans within the US economy and indeed most western advanced economies; Asset Backed Securities. Once again i'll be focusing on the US as it has the most data available and is emblematic of the problem, but Europe suffers much the same problem, though it's more hidden across language barriers.

A mortgage backed security is one form of asset backed security, where the assets ultimately are houses, sliced up into fractional slices. Car ABS is another easy one to understand, as those are fractional slices of car loans ultimately backed by cars. Student loans are another, where the asset backing the loan is either a government guarantee or private assets of co-signers on private loans.

As you might've noticed, the general theme here is "loans", and thus debt. While asset backed securities ultimately are backed by asset collateral, firstly they are backed by the debt that person incurred obtaining the asset, and the ability of that person to pay back that debt.

It's here that i have to link yet another one of my older articles; The Problem Is Too Big:

I already discussed this very subject there, though with the passage of time there's some new numbers out that i'll use to summarize the article. In fact, i'll make it as simple as a picture book:

This:

Has to be paid for by these people:

Which, along with the corporations they receive their wages from, are responsible for this total amount:

And when that's dealt with, they'll somehow come up with the cash for this:

In short, the United States is broke.

EVERYONE seems to have magically forgotten what Debt is. It's not a gift. It's not magic, either. Debt is an amount of money somebody gives to you with the explicit understanding it's going to come back at some point in the future.

Debt that doesn't have to be paid back is worthless to the lender.

Equally, debt that can't be paid back is also worthless to the lender.

And the debt incurred by the people above is what is backing all the assets within the US financial system. Yes, USdebtclock.org where these screenshots are from also lists "National Assets", but i refuse to screenshot and link that. For the simple fact i've made screenshots before, and i can tell you that the moment the US stock market drops, those national assets evaporate just as quickly. GDP contracts, but debt doesn't, unless it's paid off or defaulted on.

Truth is we've become so financialized, we have no idea how much everything is truly worth. Using mortgage backed securities, you can hide the poor performance of loans by sticking them with good ones, and selling the whole package as "diversified" and "Triple A". We learned this lesson the hard way in 2008.

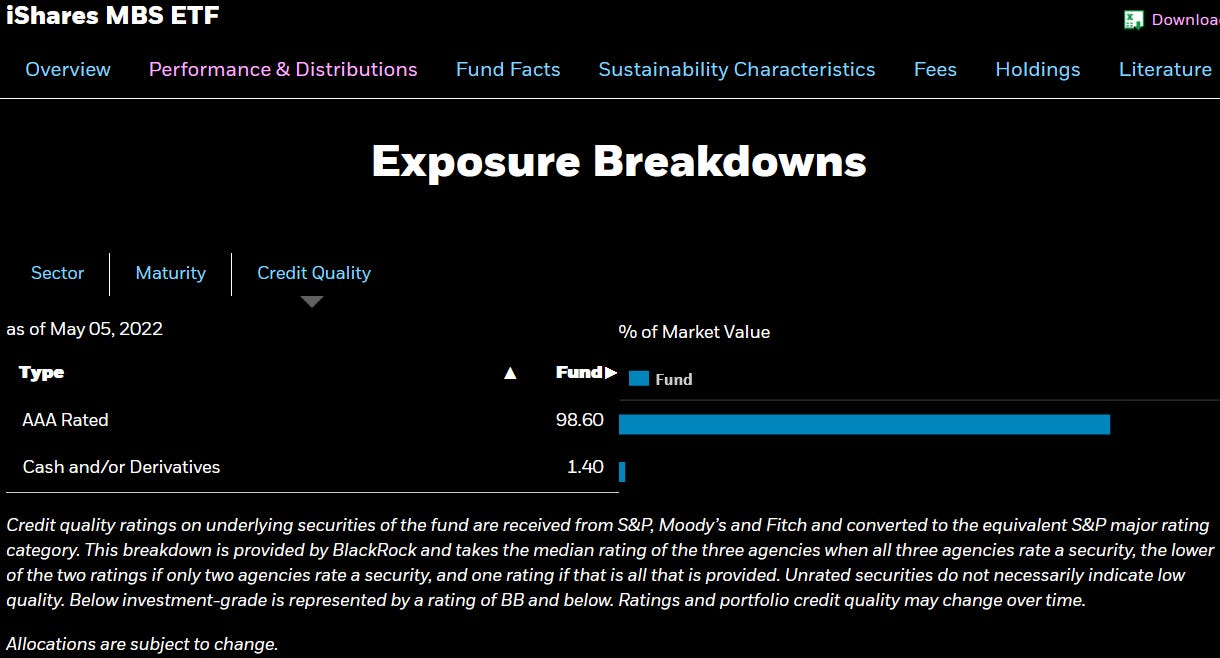

Or did we? Because, when i dug into a triple A mortgage backed security ETF, i found something much different:

This doesn't look very triple A to me. However, this is what comes up when you look at the Supplemental Holdings list that one can download from iShares own website; which is also where the credit breakdown comes from:

https://www.ishares.com/us/products/239465/ishares-mbs-etf?qt=MBB

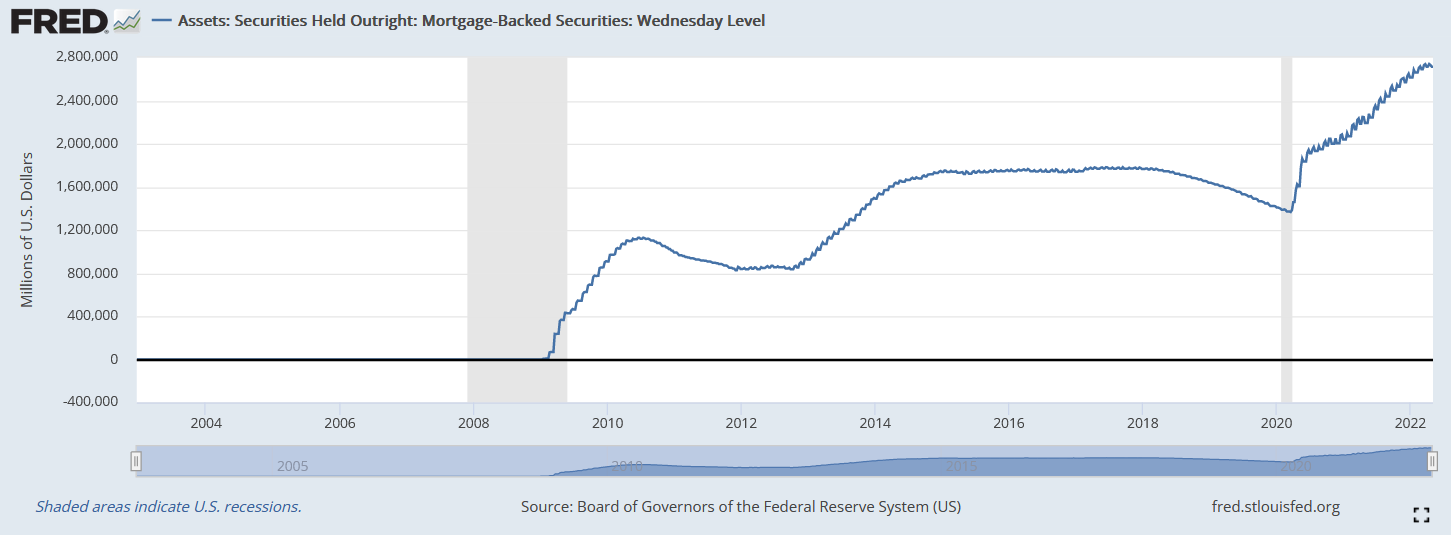

Now, i have no way of looking into the individual MBS and look at the slices like Michael Burry did. And many of the names of MBS in MBB say or show nothing about the credit scores. However - if rating companies have the balls to rate <660 FICO loans as triple A - which they MUST'VE DONE in order for MBB to list itself as AAA - then i have zero faith the loans backing the MBS with a name that doesn't tell me anything actually contain better credit quality. Especially not after a decade where the Federal Reserve bought MBS sight unseen, leading to a massive $2,7 trillion dollar MBS balance sheet:

They cannot possibly know what's inside $2,7 trillion worth of MBS, even if each contained individual loans, let alone thousands of slices of loans. It's too much.

I might not be able to look at the data directly, but i do have logic. Considering the Fed literally bought whatever to stabilize the system, it's logic to unload your worst shit to the Fed first. So i can already guarantee whatever's on that balance sheet is worse than what's in MBB, as it's a black box.

And it's also backing the value of the dollar now. Central bank assets are fiat currency collateral. This includes the US's gold reserves as well, all 8000 tons of it... Which has a present value of approximately $500 billion at current day market rates.

Which can easily disappear down that $2,7 trillion dollar black hole (without a sudden revaluing to make gold out-price the bad shit that is) - and that's not even discussing government treasuries, which we'll get to shortly. This is the reason why in my recent video discussing MBB i said that auditing the Federal Reserve's balance sheet is very quickly going to become a matter of national security, as the Federal Reserve is in real danger of going bankrupt! They might have to write down more loans than they have counter party risk free assets like gold or foreign currency reserves! (and that's not considering the ECB's, BoJ's, or BoE's black holes).

For a more indepth explanation about MBB and the coming housing crash, the video can be found here:

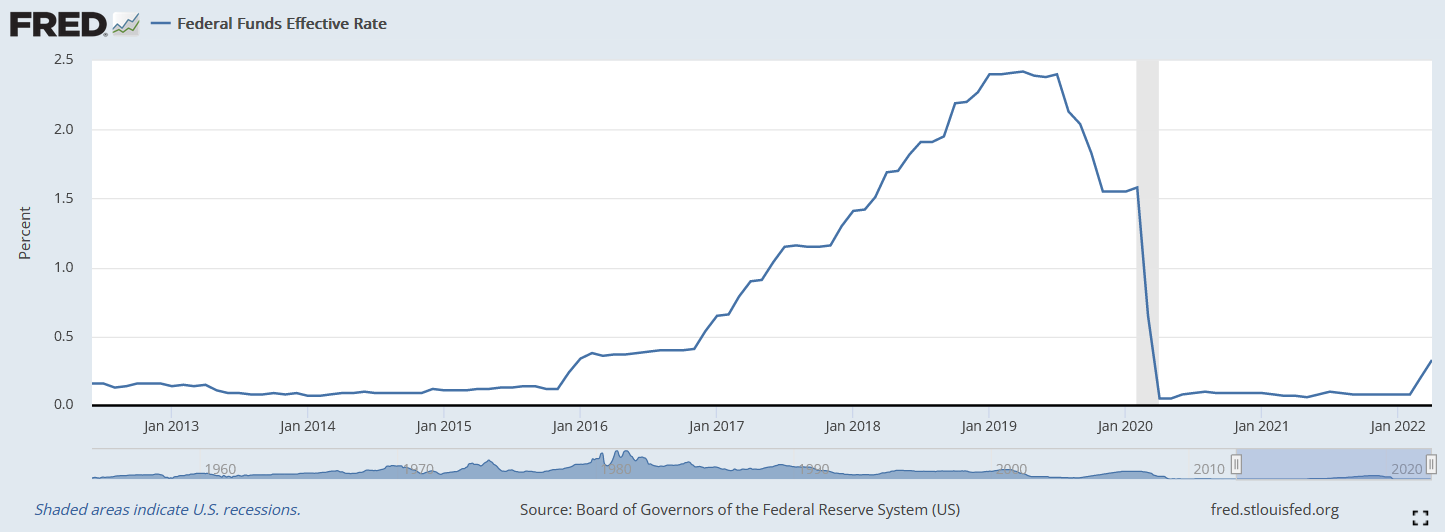

Which also explains the reason for why everything is taking a nosedive now; because the Fed is raising rates and tightening the balance sheet. The reason they're doing that is because they're about to lose control of interest rates and the bond market altogether, and they have literally no choices left. This is something i've been warning about for a long time, even doing a video about it with Rob Kientz at the end of January:

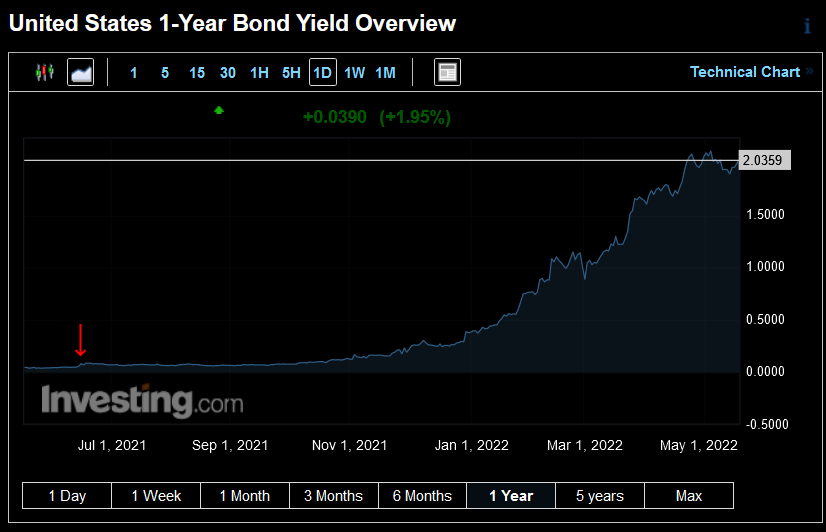

Though at that point it serves more as a history lesson as one only needs to pull up a bond chart to see it for themselves:

And compare that to the Effective Federal Funds Rate to see how far "behind the curve" the Federal reserve actually is.

I've picked the 3 year specifically as the shorter end of the curve trades closer to the effective fed funds rate than the long end, and the 3 year currently shows the biggest dramatic spread to illustrate my point. So many pundits missed this collapse in bond prices because they were looking at nominal rates in a historical perspective, where rates went from historically low to historically just-a-little-less-low, while completely missing comparing patterns between the 3 year and the FFER.

After the initial taper tantrum in 2013/14, the bond market played ball and rates went up with the FFER. Now, in 2021 and 2022, the bondmarket has been leading the FFER for a very long time. Where previously the bond market still waited for the Federal Reserve to set the rates, it's no longer waiting, and making decisions on its own.

I've written about this before as well, about how manipulation doesn't mean you can control a market - you are only the dominant influence within it at that time. And that can also only be done by attacking "chokepoints", or key tradeflow points within the market where most price action relies on, or using weaknesses within the system we have to simply hide data from the general market so it doesn't interact with the market's price setting mechanism.

Using how we started this article with the explanation between money stock and liquidity; if you can force money into an account out of the economy that it cannot leave or won't leave, it won't change the overall money stock, but it does change liquidity and as such, shows up as deflation as liquidity drops (which is how Reverse Repo has been countering inflation by hiding nearly $2 trillion of currency through offering a risk-free return). You can think of everything in the same way: The "money stock of MBS" is how many MBS are truly out there, while "MBS liquidity" is the amount of MBS "available for trade".

So if you buy all the bad MBS in the market and hide them on the Federal Reserve's balance sheet (an account where things don't necessarily have to flow out from), then no bad MBS trade in the market (and the nominal number available for sale goes down), making whatever's left more valuable. This raises the prices of those MBS left, and makes it look like they are far more valuable than they really are.

So that's where we are, and that is the true source of all our woes. We ran out of good collateral years before 2008, and started repackaging shit while hiding it was shit through buying off the rating agencies. That came back to haunt us, but rather than taking the hit and letting the system delever, ungodly amounts of money were printed to both hide this shit on the Federal Reserve's balance sheet so the market wouldn't notice, and nobody got punished for it, leading to massive amounts of "moral hazard" on where the QE money went, while the regulators deliberately slept at the wheel as any reversal of any of this would've collapsed the system. Ponzinomics was the only way out.

Moral Hazard's a term you might've heard in the past (but not for a while, guess why), as in the past it was often said QE would lead to mortal hazard - meaning, people would no longer judge investments on their value, but use the easy money to speculate as more easy money would cover any losses. Well, it did, and because the people who did so got away with it, they started doing it even harder.

Which is what explains MBB having below investment grade bonds rated as triple A inside. Nobody ever cared what went into the bonds, or even what went into the ETFs, as no one ever looks when times are good. Another lesson i thought we would've picked up from The Big Short, considering the fucking movie starts with "How did they do it? They looked."

Well whatever, guess that means i get to be the next Burry where so many others wanted to. Though i prefer Mark Baum to be honest (while i'm going to end up the Rickert of this story at this rate). If ya need proof, here's me talking about MBB in March 2021 during the height of the housing mania:

Though it got much less traction at the time than the recent video about MBB. I guess The Big Short 2.0 should start with "In a mania, nobody wants to look". It's not that people didn't think to look. It's that people actively didn't want to know. The data is there. I looked.

MBB is the best example as it's raw data available to all, and simply put, they fucked up on the bond names. As Jared Venett said, "Yes, there's some shady shit going down, but trust me, it's fueled by stupidity". I wouldn't have found out if iShares hadn't been arrogant or stupid enough to put bonds with the FICO score in the name in the ETF. Again, most names don't tell me anything. Logically i might've drawn conclusions, but i wouldn't have been able to show them. Though technically, they ended up getting away with it, considering MBB collapsed with nobody (but me) noticing, and now everybody's stuck holding the bag as demand tends to be at an all time low when the price is too.

And if MBB hitting a new all time low wasn't enough concern/evidence for you, here's a triple A CLO ETF starting to slide (and yes, despite the propaganda, there is no difference between CLOs and CDOs). Remember, if something continually goes sideways, and then stops doing that, that constitutes a pattern change no matter how small it is. Big things have small beginnings:

But the same is true for other asset classes as well. Here i can link what's technically the earliest article i've written, but i had nowhere to put it at the time. It's something that i was looking into for inflection points on the original financial crisis before Covid messed up the timeline: SLABS, or Student Loan Asset Backed Securities:

Considering i had nowhere to put it, i figured i should upload it somewhere some people could get some enjoyment out of it. And i'd come across the student loan defaulters reddit while doing research into whether or not it was really impossible to default on student loans. TL;DR: It's not. People have defaulted on them and won court cases to be allowed to default.

The gist of the article is simple: I came across research that showed that the government guaranteed student loans, the so called FFELP loans, were severely curtailed after the 2008 crisis due to fraud with them. However, Sallie Mae, the main corporation issuing student loans, hadn't gone bankrupt in the crisis and hadn't been bailed out. Infact, they were still in business, and business was good, so what gives?

It turns out that in 2019 already, about half of all student loans weren't government backed. They were private student loans, in which case the loan has a co-signer on it, usually a parent (as students have no creditworthiness) and the loan is backed by that co-signers assets such as a house or a car.

Oh yeah, it didn't take me long at all to reach the conclusion you're reaching now. You can see the government guaranteed loan as triple A rated, as it's guaranteed to give you your money back even in case of default. The private loans are then AA to B, depending on the creditworthiness as well as the asset values of the co-signers.

And since the triple A good stuff was restricted, while student loan debt has been a linear line straight up, it doesn't take a genius to figure out they've been cutting up SLABS with ever fewer slices of AAA and ever more slices of shit, just to increase the volume. Lord only knows how bad that problem has gotten after the US government basically put the whole thing into forbearance at the start of the pandemic. The student loan forgiveness that's talked about now will be much more about the Sallie Mae Corporation not going under than saving people's futures.

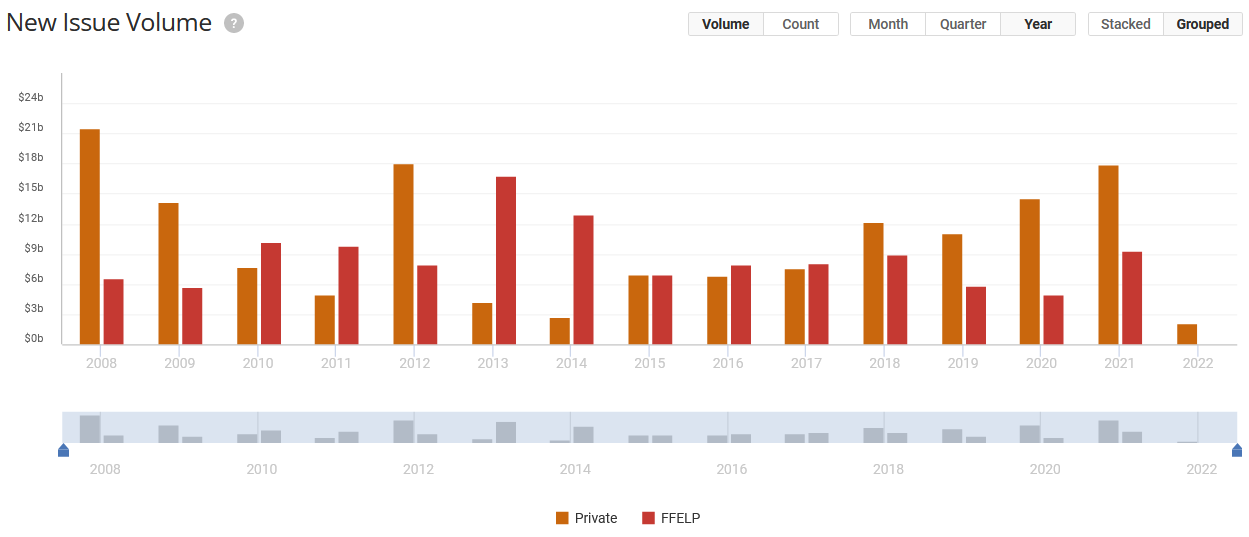

That can easily be shown by an overview of FFELP loan issuances that i found:

https://finsight.com/student-loan-ffelp-abs-bond-issuance-overview?products=ABS®ions=USOA

Note that this is just student loan issuance, private or government backed, and not the volume of SLABS. It should be enough to show that private loans are just as big, if not a bigger part of the student loan market, and it doesn't take a long leap of logic to consider these loans have been securitized (read: sliced with shit) like literally every other asset backed security.

I could go deeper into SLABS, but while looking around i ran into this longer research paper that was published not long after i wrote my own article on reddit. Somebody did ask me to compare notes at the time, but i had to decline considering the reddit article was literally all my notes (as people these days know, i don't hold back) so i doubt it's related. But it just goes to show i wasn't the only person looking into this at the time. The research paper can be found here:

https://scholar.smu.edu/cgi/viewcontent.cgi?article=4867&context=smulr

I could go on and on about the different asset classes, but i think my point here is made. Worthless shit is permeating our system, and by our own actions, we have NO CLUE what is and isn't shit. But, as the debt statistics i've shown above give away, the one thing we CAN determine, is that there's a HUGE pile of shit.

Debt HAS to be paid back, at some point. If the debt cannot be paid back, the debt is worthless. We've got a metric shitton of debt, with no way to work out what is and isn't going to come back, especially not as more people lose income causing cascading debt failures; but we can safely assume most debt won't be repaid by analyzing the creditworthiness of the people holding the debt. At that point, we were already living on borrowed time. And it might've been able to last a little bit longer....

...if we hadn't shut global supply chains down with Covid and jump-started a wage-price spiral with inevitable price increases. We could've taken 1 lockdown for 2-3 months. That causes a supply shock, sure, but that's why we have buffers. As i've said before, it's only after the raw resource producers run out of buffers without any pause to refill inventory that bids move to an auction process, and the supply shock starts traveling back up the chain, raising prices all along the way. Margin compression slows that down a bit, but by then it's already too late and emergency rate hikes become justified. Raising prices causes people to demand a greater share of the currency generation, which they'll get if things like food and rent run out of control, which leads to said vicious spiral.

Make no mistake, it would've happened anyway as product lead times would've naturally become longer and longer after the next financial crisis. But things would've slowly start to run out, rather than everything running out at once due to supply constraints and demand panic. It would've been more gradual like Venezuela or Turkey (the latter is still "in the process of collapse", not even within collapse, to everyone's surprise).

So the stage we're in now is a predictable stage along the road to hyperinflation, and one i've been warning about. Naturally, as too much liquidity circulates within the economy and rates start to ignore the central banks, they would move to do something about that. If a central bank loses control of interest rates, they're effectively useless, as that's all they can do. Set rates and print money. That'd lead to a crisis of confidence and hyperinflation by itself.

This is the stage where they find out they can't do anything about inflation. Because of their previous stupidity having driven them into a corner. Or as i've been saying; stuck between a rock and a hard place with their backs against an unmovable object and an unstoppable force coming their way. There is no way out.

They will raise rates and even attempt to run off the balance sheet because that's what (their) classic theory says they're supposed to do in a situation like this. Like a bunch of buffoons though, they don't understand their own theory. They're not intelligent and capable of adapting the theory to the current situation, they can only regurgitate what they've read in outdated books. And memory isn't intelligence.

So let me explain both the theory and their mistake then, though note at this stage there is literally nothing good the Federal Reserve can do, and even doing nothing won't lead to a good outcome. It's as futile as having regrets after having jumped off a building but before having hit the ground.

The Fed's theory in this works on the basis of liquidity. Since they added money to the system by keeping interest rates low and engaging in QE, they now need to engage in raising interest rates and QT to do the reverse. This is also an implicit admission that QE is inflationary, by the way. As higher interest rates makes it harder to lend, less new money is created through levered up principal and interest. While the amount of currency created per loan goes up because of higher interest rates, because it's the people that have to come up with the additional money to afford the interest rates, their lending capability drops faster than the income from interest rates goes up. Hence, less new money is created, and with a credit based society, since it becomes harder to lend, a recession ensues.

QT then as the reverse of QE sells bonds into the market rather than buying them out of it - through their current plan is slightly more refined; they're planning to let maturing bonds run off and simply not replace them on their balance sheet by buying new bonds in the open market. So technically they're not selling anything, they're just removing a buyer from the market that is still in currently. So yes, even while they said QE has stopped, they're still buying bonds, in order to maintain the nominal number on their balance sheet as bonds mature. That'll end with QT.

However, this all shows exactly why they don't even understand their own theory, let alone what's happening in reality. They act as if liquidity is this homogeneous pool of capital that can switch between any asset at any given time, but this isn't true. Money in your checking account for food is counted as liquidity as it's money that can and will travel through the economy - but it won't start its journey through the economy by buying US government bonds! While Liquidity as a concept is very much true and important, liquidity per market is what matters here (the apples/pears example above). I've talked about this often enough by explaining Location of Capital: Who has the excess liquidity is very important.

Considering the money was lent by the US government and spent into the US economy, that money's diffused through the entire economy now through social programs, and will not return to the bond market 1 to 1. And the US government is still lending and spending into a deficit, so it's not like the money can come from the US government through taxes either. That'd require a tax surplus, which the US is never going to see again at this point in this financial system.

And it's this very fact that changes the game. The person who lent the money off the Federal Reserve to create the bonds on their balance sheet, cannot possibly pay it back, and infact is on track to lend $1,4 trillion more than they're taking in just this fiscal year. With trillion-plus deficits projected for the next decade in the best case.

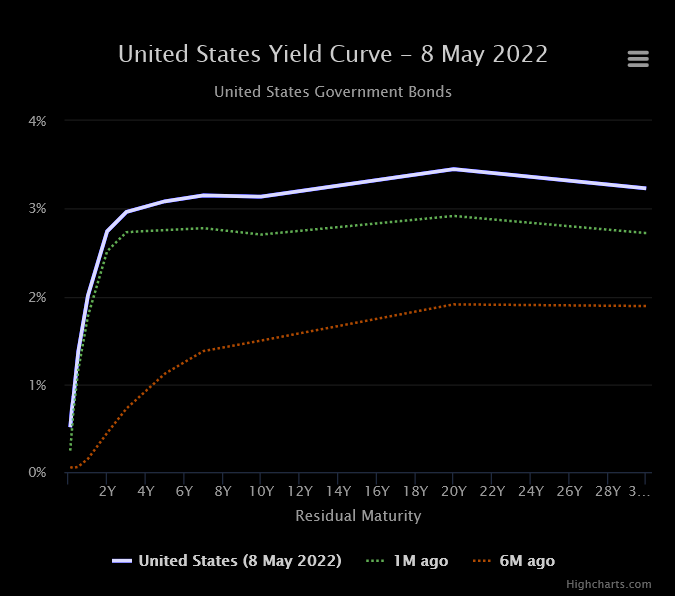

If the debt cannot be paid back, it is worthless. The US government objectively cannot pay it back for the next decade, and predicting further out in this uncertain environment is pointless. We know they're going to create more debt. The ONLY reason rates went down last year and are still relatively low now (as well as the current correction), is because of the utility value of US treasuries. For the longest time, they were considered "the safest asset on earth" because 1. The US always pays its debt (which is what the politicians are solely focused on), and 2. Because rates were going sideways or down.

In that case, bonds function like any other asset. Bonds have 2 components, the price and the yield, which are linked and inverted. The lower the price, the higher the yield, the lower the yield, the higher the price. So considering we were in a 40 year bond market with yields continually going down, it conversely meant prices continually went up. I've seen comments of bond traders over the past years saying that "the coupon does not matter", meaning the interest paid on the bond, as it was tiny at these low rates.

At that point, it's literally about buying $1000 and selling that thing for $1100. All that matters is making a profit on the spread over time, and as long as it's not moving downwards, it really doesn't matter what is being traded. That goes for crypto, metals, or debt. That goes for literally every asset that has a market where you can buy and sell it, regardless of the asset's function. If you are guaranteed repayment, then you cannot lose your money that way. The only way to lose your money, is to buy a bond high and sell it low.

US Interest rates stayed at 0% for half a decade, rose to 2.5% which broke the markets, and were halfway to 0% again before Covid hit. The question of "why now" is simply answered by the nominal rates on bonds, which over time went all the way to nearly 0%. The Federal reserve excluded going negative, while Europe having gone negative rates for half a decade without any success would've made any success there short-lived anyway. Clearly, negative rates don't work, and the reason why is fundamental.

The interest rate on a loan is an expression of risk. It's not some magical rate that we determine to be so without any further ill-effects. It is there for a reason. And the reason is that all loans, no matter how small and to whom, carry a risk that the money won't come back. There is no such thing as a risk free loan.

So there certainly isn't a negative risk loan!

Which is what a negative interest rate indicates. It's beyond a guarantee that your money comes back. That simply cannot happen. Hence, if the interest rate on a bond goes negative, it can only be achieved through supply and demand manipulation. As i've stated before, supply and demand works on debt just as much on anything, so if you just buy up certain loans en-masse and hide them outside of circulation, the price of the remainder of similar loans increases due to scarcity, which conversely drops the linked yield.

Which is how the Federal Reserve and all central banks have kept yields artificially low for years, by restricting the supply of bonds by hiding the excess on their balance sheets. And since we know the Federal government cannot run a surplus and thus will lend more, any bonds the Federal Reserve doesn't buy through QT, must be bought by the market.

In short - they're counting on demand for US paper that hasn't been there since 2008, otherwise they would've never had to start QE to begin with!

2014-2019 was a short reprieve for the system, but the US was already done for by then, the market floating on liquidity previously created. Ever since the repo crisis in late 2019 it has become impossible to turn the printer off, because this exact situation that we're in now - a total collapse of credit based collateral - would've happened at any given point if they did. But now the can's run out of road, and the collateral's going to collapse, because there's simply too much rotten collateral out there and we don't know which is which. Too much junk got rated triple A, and now we basically have to go through a mountain of needles to find the haystack.

I've got tons of signals coming from the market that clearly show how QT is the policy error the Fed is making through signaled expectations - and at the same time prove that i've been right all along in pounding the table about the debt problem having become too big, and all roads leading to hyperinflation to get out from under this debt.

The first rumor about QT being a possibility, and at a faster clip than before, came out on January 3rd 2022. Though the Fed was hawkish on rates before that - that's when they started the "market reaction" to QT, to see what it would do when the rumor hit.

Well, MBB:

The US 3 month:

And most other credit ETFs and instruments basically look the same. Even though there was already a decline on the way, the announcement of QT severely hastened it, and has been the number 1 reason why the bond market has stopped listening to the Fed altogether (while the Fed still pretends it does). Because the Fed has basically announced the end to the party, and the market will now test its resolve all the way back to the mean of when that liquidity started (2008 levels).

The market can suffer much higher rates, IF the Federal Reserve keeps buying up the bonds. Because, what do we care if the Fed buys trash at 1% or 10% interest rates, as long as they continue to buy the bonds at face value? Sure, the actual price of the bond might be much lower, but hey - that's why i keep calling the Fed's balance sheet "Schrodinger's balance sheet", because as long as you never look at what's on there, it holds its face value.

It's also because of this reason that i expect the Fed to eventually raise rates and QE, to stop general inflation by making lending harder through higher interest rates on credit, but at the same time bail out the asset holders once again to hide more shit on their balance sheet because they're going to have to. Just look at JAAA or MBB. And since they've so far refused to explicitly acknowledge that QE causes inflation, that's the excuse they'll use to claim QE won't cause more inflation ("we didn't have it before 2020! it's supply chains guys! it is!"), while the reduction in lending "will" cause inflation to settle down.

However, i expect it to have the opposite effect. Because we know the creditworthiness of the US is basically zero at this point, all that matters is the supply and demand mechanics of the bond market now. It's just another token being traded. If more bonds are added to supply, for example because the US government needs to continue to lend to afford its social programs, yields will rise. This, again, because yields and prices are inexorably linked, but there's one aspect of pricing that Jerome Powell and the rest of the Fed simply don't understand, because it's run off demand, not supply:

If nobody wants to touch the stuff, the seller must drop the price, until a buyer is found. "Price" doesn't exist, it is simply the last number the last sale was for. A market can go bidless, reducing the price to zero instantly. Just ask any crypto trader at this point. Once they stop accepting bonds on their balance sheet, it's not going to be long before yields explode as liquidity dries up, and the Fed has to restart QE faster than before to stop the market from going wild, pinning rates with Yield Curve Control.

And while i don't expect US treasuries to go bidless, i do expect general market demand to continually overwhelm whatever QE program the US institutes. Any given number the market will overwhelm in weeks or months, just to force the Fed to accept more bonds on their balance sheet and bail everybody out at a higher price than they're willing to pay each other in the open market for the bonds. This is where the manipulation bit comes back into play; the manipulation only holds as long as you can hold onto the chokepoint you're influencing. If a flood of bonds rushes the market, either yields go to triple digits, or the Fed buys it all and the dollar's purchasing power cuts in half, with no in between.

A similar thing is already happening to Japan, because the numbers are an order of a magnitude or two larger there, with over a quadrillion (1000 trillion) of debt owed by the government, the vast vast majority of which to the central bank. Should interest rates be allowed to rise, the interest that needs to be paid on that pile of debt becomes so large so quick, the country goes bankrupt overnight. The only solution is to do what the central bank is doing, buy unlimited amounts of bonds and destroy the currency so that the debt may be paid back more easily. Save the bond market by destroying the currency, at faster or slower rates depending on how much is panic sold on any given day. Which means the "exponential" phase of hyperinflation has started in Japan; though as always this takes place over months and years, not days. Things might seem calm for a while before something pops up again to accelerate the situation.

I decided to start writing this article when i came upon the first evidence that this was going to happen to the west. I mean, sure, i can show yields going up and MBS prices going down, which clearly indicates a problem (and now JAAA further confirms CLO problems). As always though, why wouldn't the Fed be able to solve it like any time before, and just continue to buy the bonds? Why should QE no longer work? WHEN has it been "too much"?!

Well, in my mind, when other people refuse to touch the stuff unless the central bank buys it. Where even dealing in the stuff becomes too risky, and you don't want to be left holding the bag when the music stops. And i found just the chart to indicate this (from https://www.sifma.org/resources/research/us-asset-backed-securities-statistics/):

I doubt i need to explain this chart, but let me do so anyway. It clearly shows that, since December 2021, Collateralized Debt Obligations/Collateralized Loan Obligations issuance has taken an absolute nosedive. This is another chart that clearly indicates QT as the culprit, as the Fed was already revealed to be more hawkish than previously thought in their November meeting, in mid-December. Yet, December still ended as a blow-off top for CDO/CLO issuance.

Finsight's another website that tracks ABS issuance with a whole bunch of data (though SIFMA seems to collect more data on the backend) that also shows a marked decline in CLO issuance:

https://finsight.com/all-abs-market-bond-issuance-overview?products=ABS®ions=USOA

Come January, where the rumor of QT started at the very beginning of the month, CDO/CLO issuances completely fell off a cliff. This is not correlated with the sudden rise in interest rates, as the majority of that move happened after the war in Ukraine started at the end of February. Between the start of January and the end of February, the US 10 year basically went sideways, so mortgages had not yet risen enough to create enough demand destruction in the housing markets. If anything, it caused a temporary surge of people locking in lower rates in the face of higher ones, so if anything CLO issuance should've increased.

At the same time that MBB started falling, and the US 3 month yield started rising, CDO/CLO issuance dove off a cliff and basically ended. That can't be coincidence. Not to mention there are signs in the longer dated yields such as the 1 year from the middle of June 2021 that things were already changing (the bump was significant at the time but seems much smaller now):

The bond market is smarter than the stock market, and it's screaming as loud as it ever has that this party is over, that THIS IS IT, and the music has stopped.

What all of this means, is that the collateral underlying the financial instruments is finally going bust. This being the US tax payer who has student debt, car debt, housing debt, credit card debt, personal loans, business loans, payday loans, downpayments and medical debt.

Debt has to be paid back. Rather then focus on any one sector, how is the US tax payer going to pay back all of it?

They can't. As such, the US government bonds (local, state and national) are worthless, the mortgages are worthless, the car loans are worthless, it's all worthless until you've figured out who can and who cannot pay. As long as you don't know who's going to take the hit, everybody will try and insulate themselves as much as possible via a Tragedy of the Commons sense of self preservation; meaning spending drops while safe havens soar. As more people cannot pay taxes (or are unwilling to), the national debt needs to be borne by fewer and fewer people who can actually pay. This will make an impossible situation more impossible, and increase the yearly deficit yet further.

Defaulting on the debt is the end game in every respect, but it can't be done upfront, as it immediately stops the government's ability to lend and thus the US government would have to immediately cut $1,4 trillion in yearly spending; and then cut more when the effects of those spending cuts drop tax receipts like a brick. Armageddon is simply not an option, hence that central bank bond buying is the only option.

And that is a situation that can never fix itself. It is the end game of this financial system as currency floods it, and we will see multiple Western economies go Weimar. It is the very same reason Russia is moving post-haste to a commodity backed currency, the war sanctions having given them a bigger incentive to leave the current system than to stay it in. The new system does not carry these issues of mistrust, as it runs on pure commodities, not financial derivatives (commodity backed securities are slowly going bad too, thanks to events such as the Nickel squeeze diminishing trust in futures and trading houses like the LME among traders).

You don't need to figure out whether or not a gold-backed currency has value, you only need to figure out if the owner has the gold they say they do. If they do, and the currency is freely convertible/redeemable, then the currency has the same properties as gold, and will hold its value even when debt based currencies do not (at equal supply/backing). Obviously, the demand for a stable currency when all others aren't stable should push it past intrinsic value and into a premium, which is also the incentive for other countries which are capable of doing so to switch over to the new system; while the countries and currencies which don't switch start getting discounted more and more, forcing yet another vicious cycle to occur.

While we in the West could reform our system towards sound-collateral again, and it wouldn't even be that hard: Outlaw MBS and sell individual mortgages again; the losses we take during that process are sure to make us as a society very poor. We're talking pre-French revolution levels of poverty, as that's the amount of labor value we pulled forward with debt previously, and then refused to pay for, electing instead to consume that value and waste it on unproductive temporary things.

The financial future forward is now set. While the path forward had already been determined, the details often have to be fleshed out, which has now happened after the US labor productivity report smoked Jerome Powell's credibility right after he said that the Federal Reserve doesn't have a credibility problem, as well as set the path forward in rate hikes in stone (which has since been backtracked a bit for obvious reasons).